Holidays are a special time. Seeing loved ones, making memories, and exchanging gifts. As November rolls into December, merchants ride a wave of increased sales – which can, unfortunately, crash-land into a mound of refund requests come January-March.

So-called “chargeback season” can put a dampener on profits; when customers count the cost of overspending, sometimes it’s merchants who take the hit.

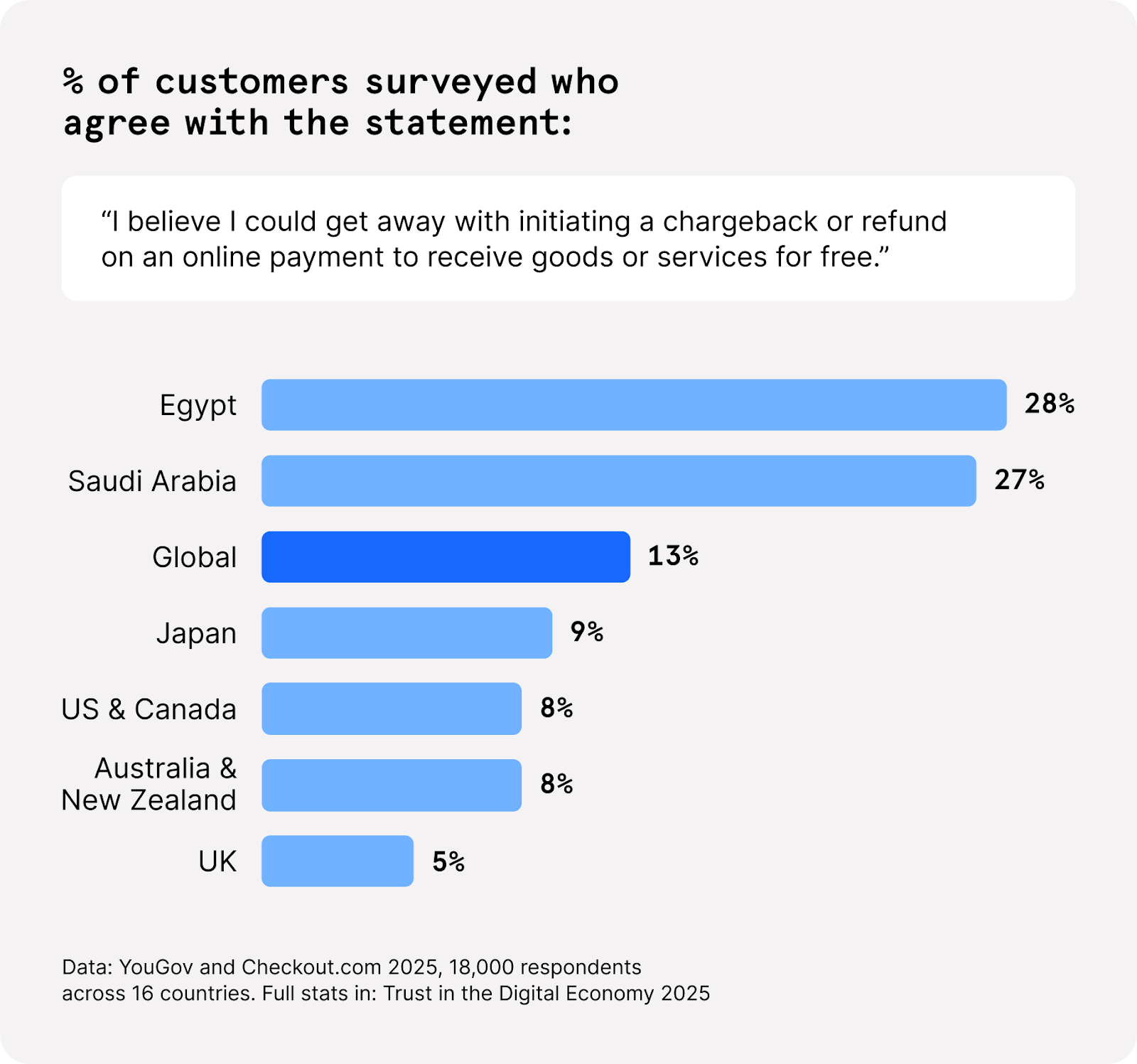

More than one in ten (13%) consumers believe they “could get away with initiating a chargeback or refund on an online payment to receive goods or services free of charge” according to a 2025 YouGov survey for Checkout.com. This is a clear example of friendly fraud: a type of first-party fraud, which means the consumer is using their own credentials to wrongfully claim funds back from your business.

But you are not powerless. Your holiday season payments strategy can make a difference to your margins. To make sure your holiday sales revenue rise isn’t demolished in Q1, you’ll need to focus on three main things:

- How you authorize payments

- Which customer data you collect

- Your post-purchase analytics approach

This deep-dive will look at all three, in turn. Along the way, I’ll also cover some strategies to prepare for the busy holiday sales season that fight friendly fraud, and curb the influx of payment refund requests in January-March.

Weighing the cost of conversion

Even though there is a drive to maximize conversion – particularly around the intense holiday sales period – profitability is still important. You’ve got to take a balanced approach to addressing the risk of revenue loss. It’s critical to consider the cost of processing chargeback claims and refunds, which could occur in higher numbers if you have minimal authentication checks or other purchase validation protocols.

Your risk appetite for friendly fraud should account for the costs of your product or service fulfillment. For higher-value purchases, it may be worth slowing down the pace of checkout in light of the financial risk; If the customer later wrongfully claims a refund, you face card network charges on top of the logistical and inventory costs. Every chargeback comes with a flat fee – no matter which payment services provider you use.

Holiday sales season increases the pressure of winning customers. The throughput of transactions – and, therefore, a lower level of friction during the authorization process – may be a higher priority for your business than preventing chargebacks later down the line. It depends entirely on your business strategy. Either way, you must carefully calculate the potential costs of rapid checkout when custom turns to chargebacks a few months later.

Takeaway:

- Large-value purchases: rigorous authentication is critical to loss-prevention later on

Reducing confusion over transaction records

Even for smaller basket sizes, the risk of friendly fraud may still persist. If you are selling through a third-party marketplace, using a parent business to take payments or making sales via another platform, then consider if your billing descriptor is clear enough. Over the holiday season, customers are typically making a far higher volume of purchases, potentially from multiple vendors. When the customer looks at their list of historic payments, will they recognize that charge from your business? Even a “small” charge that seems out of place may incur a chargeback request in a few months’ time if the customer cannot connect it with a genuine purchase. This busy time of year can make it even easier to forget the name of a business you made a small transaction with.

To reduce the chances of your customer raising a payment dispute out of confusion over the name on their transaction records, do the following:

- Send an email to your customer with a receipt of the transaction, including the amount, date, and your business name. Do this after each and every transaction, so the customer can search for it later, if needed.

- Clarify that the name on your customer’s transaction records will match the trading name of the business. Contact your payments provider to ensure this is the case.

- If it’s not possible to match the name on the customer’s bank statement with the brand your customer is familiar with, ensure the transaction receipt clearly states both names that the customer needs to know.

You will notice that communication with your customer is a core theme of reducing friendly fraud. Hold on to this thought as you continue through the guide!

Takeaway:

- Ensure your billing descriptor is a name your customer knows

Pay attention to payment authorization

Believe it or not, the reason friendly fraud may lead to costs for your business in January could be down to how a payment was authorized in November. You can alter your authorization set-up now to lower the rate of chargebacks in the future.

There are advantages to certain payment methods over others when it comes to lowering the opportunity for first-party fraud. For example, mobile-native payment methods such as Apple Pay can lead to fewer chargebacks thanks to the collection of useful data at the moment of transaction. Often, devices such as a smartphone or smartwatch will use biometric authentication to verify a payment request. In the event of a payment dispute, this data allows you to prove a transaction was legitimate – you have a record that the customer confirmed the payment with their face or fingerprint (to name two examples).

However, it’s not only mobile payment apps which gather fraud-fighting data. Even if you mainly take credit card payments, you can still choose to collect additional data from each purchase or payment request, and send it to your payment processor. This can significantly reduce costs from chargebacks – I’ll explain further, below.

Collecting detailed data to fight friendly fraud

I recommend collecting contextual data around each payment authorization, such as:

- Device ID

- IP address

- Biometric authentication (if available)

- Timestamps

Modern payment solutions such as Flow secure transactions with device fingerprinting to detect and prevent fraud at the moment of payment request initiation. Use it to set up the types of data you want collected at authorization, and you’ll benefit from the additional evidence proving genuine customer consent to the payment.

Card network dispute resolution

Card brands such as Visa and Mastercard monitor the volume of payment disputes, fraud claims and chargebacks coming from individual merchants (as well as acquirers). It’s in everyone’s interests to keep such incidents as infrequent as possible, so card brands support dispute resolution tools to help out here.

Although it’s better to prevent disputes arising in the first place, you can use Rapid Dispute Resolution to quickly provide your customer a refund in the pre-dispute phase. This stops a payment dispute from becoming a chargeback and may, therefore, save you money. As mentioned, chargebacks come with certain fees, and it could be worthwhile for you to simply refund your customer and avoid the greater expense (depending on your business model).

Post-dispute resolution

There will be some instances in which it’s more profitable to challenge the payment dispute – which could have arisen from friendly fraud – and enter the representment stage. At this point, you need to dig up proof that the customer authorized the payment in question (i.e. that they are wrongfully trying to claim funds back from a legitimate purchase).

Evidence such as the data types above will help you out when it comes to fighting payments wrongfully flagged as fraudulent. If you know the customer really authorized a payment, you need to prove it. Only certain types of data count as evidence – you can read our documentation on challenging payment disputes to find out more.

The Visa's Compelling Evidence (CE 3.0) framework can help you win a dispute by proving the customer has a history of legitimate transactions. The key is to show Visa at least two previous, undisputed purchases from the same cardholder that share key data points with the disputed transaction, such as the same IP address or device ID.

Learn more: Visa Compelling Evidence 3.0 - Overview

Fighting returns fraud for physical goods

It’s worth mentioning that you can get everything right about payment authorization and transaction data collection, yet still face issues with first-party fraud. Merchants selling physical goods such as fashion apparel, accessories, electronics, gifts, luxury goods, and other such retailers will need to pay close attention to levels of returns fraud during holiday sales season.

When it comes to return fraud, a number of scenarios are possible, including when the payment went absolutely fine, but the customer claims the merchant is at fault for other reasons.

Here are some example situations and possible solutions:

"Since the pandemic, the retail industry has seen exponential growth in first-party fraud,” shared a large merchant industry expert. “We’ve addressed this by fully tracking the product delivery and reverse logistics process, so we have an excellent grade of evidence to provide to card networks during the representment stage of payment disputes. This has helped to strengthen our profit margins significantly, especially during busy seasons like Black Friday and Cyber Monday.”

By now, you can see that friendly fraud can arise from confusion as well as deliberate attempts to defraud. Next, let’s look at friendly fraud for subscriptions and recurring payments, which comes with specific nuances.

Reducing friendly fraud from subscription or recurring payments

While the above advice centers on payment authorization for a single transaction, there are, of course, further opportunities for friendly fraud when it comes to recurring payments and digital products.

During the busy holiday season, shoppers often make quick decisions because of all the deals. They might overlook terms and conditions and miss important details about what they're buying, especially for subscriptions or free trials. This can lead to customers regretting their purchase or simply forgetting about it – two major causes of friendly fraud.

After these big sales, businesses usually see many more customer questions and more people regretting their buys. If a customer can't easily contact the business, struggles to understand the refund rules, or has trouble canceling a subscription, they'll often just initiate a chargeback. This happens even more when customer service lines are busy.

Here’s how to prevent those problems:

Clearly communicate the purchase terms

For any recurring transactions, prominently display the terms and conditions at the moment of purchase, and ensure your customers have to actively click and accept them. This means you’ll have proof of commitment to the billing cycle.

Be aware that negative renewal options – i.e. continuing the billing cycle until the customer actively cancels it – can cause frustration that leads to friendly fraud.

After you have secured consent to take payment, communicate about recurring transactions days in advance via email (or other channels, such as WhatsApp, SMS, DingTalk, etc.). This serves as a vital reminder and helps customers recognize the charge.

In your payment notification, be sure to include:

- The amount to be paid

- The billing descriptor

- The date the transaction will occur

- How to cancel, if desired

You should also take care to avoid confusing language that might create a false expectation that a product or service is "free" when it's not. For free-trial promotions, send clear reminders to cardholders before the trial period ends. This can prevent chargebacks from customers who simply forgot to cancel.

Takeaway:

- Use very clear language at every step regarding re-billing. Clearly outline the billing cycle, exact dates, and transaction amounts.

Make unwanted subscriptions easy to cancel

This comes back to weighing the cost of conversion: on the one hand, it’s important to make the most of the holiday season “rush” and gain new customers. On the other hand, profitability should remain a priority; consider that it may cost you to process a high volume of payment disputes if certain customers experience buyer’s remorse.

I recommend you simplify the cancellation process as much as it makes sense for getting the balance right between conversion, customer retention, and managing payment dispute volumes.

If including a self-serve subscription cancellation option is not ideal for your business, then you must at least ensure your customer services are readily accessible. When customers can easily reach your support team, they're much more likely to seek a resolution directly from your business rather than filing a chargeback.

Preventing repeat friendly fraud

New research indicates that consumers carrying out first-party fraud are likely to offend on a repeat basis. A study of 4,000 consumers in the US and UK for Checkout.com found that one in four (25%) have requested their funds back on two or more occasions – despite the merchant fulfilling their legitimate order.

How can you tackle this? So far, I’ve covered friendly fraud reduction tactics from the perspective of authorization. There are also strategies that can help cut the chances of friendly fraud recurring.

Flagging customers who have claimed refunds

Keep track of customers who have requested refunds before, so that you can begin to look for patterns of friendly fraud, such as policy/refund abuse. Be careful to look out for customers who have previously had their account blocked after requesting refunds too often, who then try to set up a new account with the same payment details, IP address, email address or phone number. This may be an attempt to continue defrauding your business.

Investigating data points of the customer

When assessing a transaction for the likelihood of being fraudulent, you can investigate whether the device ID has been associated with fraud previously. You can also check the age of the email address; a brand new email address could indicate a fraudster is attempting to scam your business, whereas an older one may suggest a legitimate customer.

Identifying friendly fraud if an AI agent makes the purchase

With the AI adoption boom this year, you may be wondering how to handle the possibility of friendly fraud if an AI agent made a purchase on behalf of your consumer. For example, a customer may claim that they did not authorize a payment made by an AI agent (when, in truth, they did). In a recent webinar, Mastercard told Checkout.com how agentic transactions will be marked as coming from an authorized agent. This means the issuer will have access to contextual data showing a consumer authorized a payment made by an agent. In this way, merchants will have a defense against the possibility of first-party fraud with agentic payments.

More support this peak season

We know how important sales periods such as Black Friday/White Friday and Cyber Monday can be for you. Now you’ve investigated strategies to solve first-party fraud, why not move onto our other guides for the high-volume sales season? Our insights hub contains advice, research, and tips on topics such as customer conversion, agentic commerce, payment systems resilience, and more.

.png)

.avif)