Modernity means moving forward. And in the new sales channel of “agentic commerce”, Mastercard and Checkout.com are among the first movers. We want to get your revenue moving in the right direction, too, which could mean connecting your store to AI agents that handle secure and permissioned product discovery, purchase, and payment on behalf of your customers.

Pablo Fourez, Chief Digital Officer at Mastercard sat down with Rory O’Neill, Chief Marketing Officer at Checkout.com, to unpack the emerging tech behind this macro shift in online payments. They tackled questions of security, trust, and what this means for the traditional payments lifecycle. Specifically, Pablo shed light on the Mastercard Agent Pay Program and Agentic Tokens.

Watch: Agentic commerce: Introducing the technology shaping the future of payments

The new roles of the AI agent

We’re now in an age where a single AI agent can play multiple roles: travel agent, tour guide, personal shopper, stylist, executive assistant, and ideas machine. What used to require multiple different phone calls – and then, lots of individual web searches – now takes just one webchat with a multipurpose large language model (LLM) such as ChatGPT, Claude, Gemini, Llama or Perplexity.

“I recently planned a road trip from A to Z using an agent,” said Pablo. “I told it how far I was comfortable driving each day, what types of hotels I wanted to stay at, and which kinds of activities I wanted to do along the way. Something that would have taken me multiple hours to research took [the agent] just 20 minutes.

“We were set with an itinerary. The only thing it was missing was to actually make the bookings for me: to reserve the hotels and rent a car. We’re on the verge of making that possible. That’s the next step.” Agentic payments with Mastercard are almost here.

We’re at a brand new moment in AI evolution; the difference between an AI agent and an AI chatbot is that the agent carries out a series of actions independently to complete a complex task. Instead of just running a search on “winter hiking boots” and returning the first results it comes across, the AI agent takes into account the context you give it. That means the weather conditions of “winter” in the location you’re going hiking (after all, winter in Gran Canaria is not like winter in Alaska), your shoe size, budget, shipping preferences, and – with your permission – your favorite brands, based on your buying history.

It’s not only consumers that can use these agents to save time and carry out tasks more efficiently – businesses are taking advantage, too. With new so-called “super agents” on trial at Walmart, it’s no wonder curiosity about this technology abounds.

Can AI agents be trusted with payments?

Since the first ever ecommerce payment in 1994, technologists have focused on building payment infrastructures that humans control. Thirty years later, we’re turning back to programmatic technology to make purchases for us. Here comes the most important question: what’s the difference between a trustworthy agent and a bad bot?

“It’s a new paradigm shift we’re seeing,” shares Pablo, “We had the development of [making payments] via the internet, and then mobile payments, and now we have agentic payments – it’s as big a change as that. We are very excited to give consumers a choice of how they want to transact.”

He explains that secure payments technology like tokenization, which Mastercard has been working on for the past decade, forms the foundation of trustworthy agentic payments. Transparency around which agent is making the payment is vital, because all parties in the financial chain need visibility. That the agent could look like a malicious actor – moving through a checkout much faster than a human could – means payment providers need new interfaces that recognize an agent acting legitimately on behalf of a customer.

“We don't want to lose the human agency,” adds Pablo. “So one of the key principles is that the agent acts as an assistant to you. It’s doing things on your behalf, but you still maintain control as to what you want the agent to do for you. That's a very important component.”

How Mastercard secures AI-powered payments

The Mastercard Agent Pay Program has been built to drive smarter, more secure and more personal payments experiences, working with leaders like Checkout.com to ensure only valid agentic payments will go through. Mastercard says its Agent Pay program will deliver more secure payments experiences to consumers, merchants, and issuers. It’s an extension of Mastercard’s existing secure technology stack. Because agentic payments will contain additional contextual data, Pablo hopes AI-powered payments will see even less fraud than traditional digital payments.

Pablo highlighted some of Agent Pay’s core security features:

Tokenization

Rather than the agent using your credit card numbers, Mastercard replaces it with a token that is cryptographically secured. It’s known as Mastercard Agentic Tokens, and means if a fraudster were to intercept it, they cannot use it. Tokenization also provides visibility and traceability of the transaction across all players: the customer, merchant, acquirer, issuer, and card network. It identifies the agent as a party in the transaction.

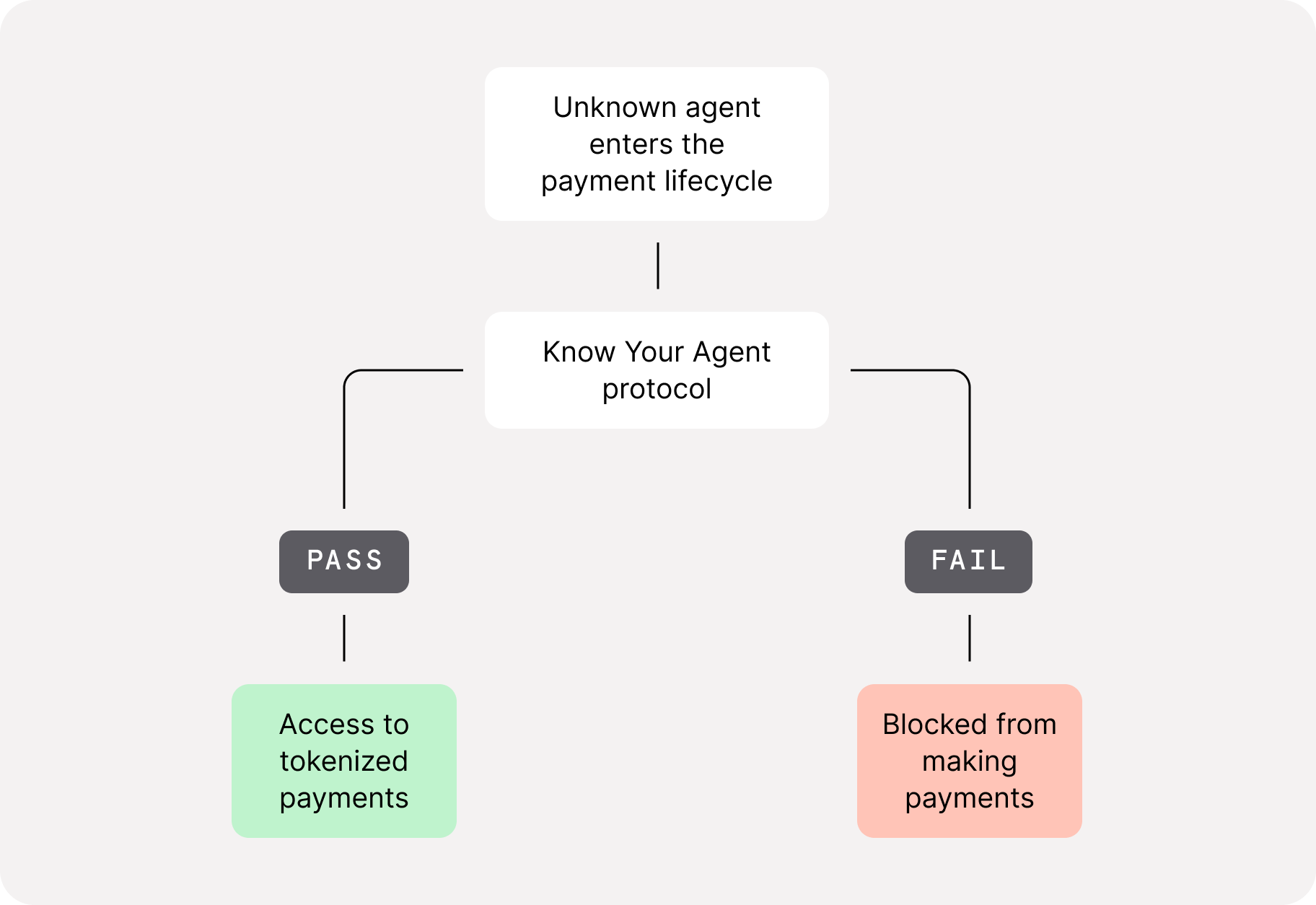

Know Your Agent

A key protocol ensures that malicious actors cannot take control of an agent working on behalf of a consumer: “Know Your Agent”. It ensures only payments from trusted parties are accepted.

“The key piece of this is, in order to get access to tokens, agents need to be registered. We have a process we call ‘Know Your Agent’ – basically a KYC process – to ensure we have good parties onboarded,” Pablo explained. “This is how we can differentiate [between a good and a bad agent] and help merchants differentiate."

Authentication

The agent acts independently – but that doesn’t mean it can buy anything, anytime. The consumer can authenticate a payment using biometric confirmation on a mobile, for instance, a fingerprint or a face scan. Other options like Passkeys and Two-Factor Authentication leave no doubt whether the cardholder consented to a transaction.

What’s exciting about Mastercard’s Agent Pay is the ability to add the context of user intent to the payment request at the moment of authentication. Pablo gives the example of asking an AI agent to purchase a specific pair of Adidas shoes, in his size, for €80. “That data is carried alongside the token to the different players in the transaction. That’s one of the key differences [between regular online payments and agentic payments] it’s enriching and carrying more data that is authenticated alongside the tokens."

Standardization

One of the things Pablo and his team need to do is to drive standardization of agent data-sharing, so that adoption is secure and reliable for all parties. He clarified: “For example, we have now a standard around the use of MCP servers that can be used to expose APIs to agents. That's one of the key things that merchants are starting to work on: how to change their interfaces so their site data is easily discoverable by an agent.”

Merchants will be able to use new standards to indicate certain pieces of information about their products or services to the agent, which would then factor into decision-making. For instance, the size of an item of clothing, the fare class of an airline ticket, or the refund conditions of a particular purchase.

Fighting fraud

Pablo explained that all the security features mentioned work together to prevent fraud. While fraudsters will, inevitably, try and take advantage of any new payment system, he said: “At Mastercard, we are definitely investing a lot to leverage these tools to detect fraud more quickly on the network and to help our customers with that.”

The higher quality data of agentic payments helps all parties to distinguish between fraudulent and non-fraudulent transactions. Even if the customer should try to attempt friendly fraud, and claim the agent made an unauthorized purchase, the issuer will be able to access such contextual validation to prove that the payment was legitimate.

Will the merchant lose their connection with the customer?

Clearly, there are big implications for the merchant-customer interaction. Indeed, agents are already disrupting product discovery and online shopping, presenting merchants with a new set of decisions on customer engagement and retention. If consumers don’t land on your website anymore, how do you structure your data for effective marketing and sales?

Pablo is aware that merchants want to foster relationships with loyal customers, and his team is working on a “logged in” experience, where consumers can still collect loyalty points and enjoy personalized offers such as free shipping. This would allow the merchant to identify the consumer, connecting them with their existing customer account, and allow for tailored product recommendations, based on their purchase history and other relevant profile data the merchant holds.

The ability to connect a customer with their personal accounts across various brands can also facilitate card-on-file payments, as Mastercard would be able to tokenize credentials held by merchants (or their third-party vault providers).

Pablo sees a wide range of diverse agentic use cases up ahead for merchants. “We're very keen to help merchants engage with consumers through this channel. I think there's an opportunity to [give consumers] a personalized experience like never before. So it's exciting. It’s worth jumping in, whether you’re an issuer, a merchant, or [a party] facilitating these transactions, as we’re trying to do, in a way that can be trusted and secured.”

“I think there's an opportunity in trying to figure out together what are the right models that makes the most sense,” Pablo added. “And from our perspective, we're trying to do a principle-based approach: we want to do things that bring trust [and] consumer choice, [through] the security, authentication, [and] the transmission of data. [These] are all things that [underpin our] objective of providing visibility, [and] trust in the system.”

.png)

.avif)