With the growth of digital payments fraud has become ever more sophisticated, and authentication has had to adapt to keep up. To improve security for both consumers and merchants, the European Payment Service Directive (PSD) has updated its regulatory standards to PSD2.

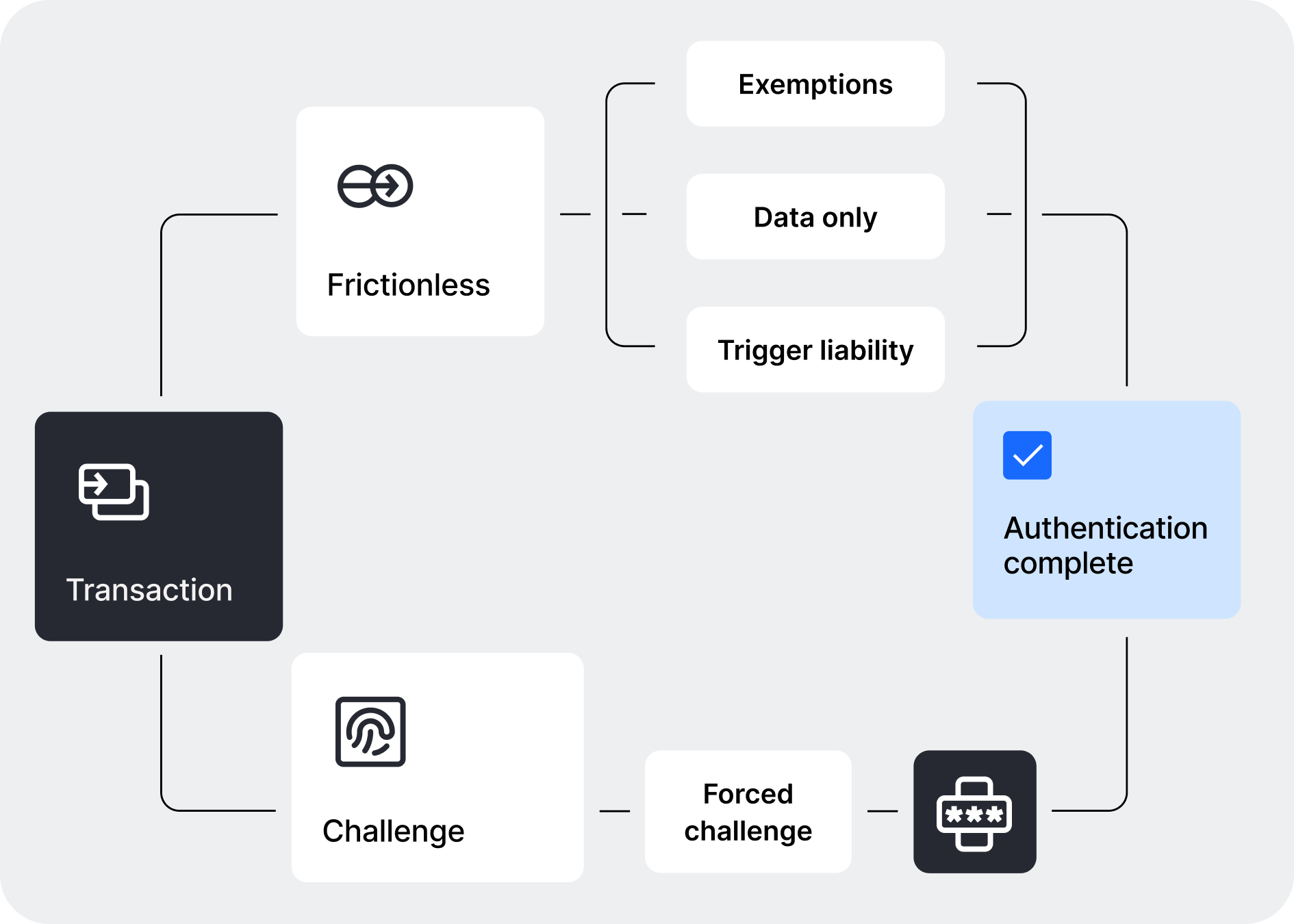

Part of this is 3D Secure 2.0, an enhanced security protocol that irons out some of the pain points of its predecessor and uses a wider range of data and biometric authentication to facilitate smoother, more secure payments.

3DS2 does this through stricter transaction security measures, including Strong Customer Authentication (SCA), Risk Based Authentication (RBA) and Transaction Risk Analysis (TRA). These improve both safety and the customer experience, helping to cut cart abandonment and increase conversions.

PSD2 SCA is not yet universally mandated, but merchants doing business in the European Economic Area are required to offer two-factor authentication as part of the payment flow in order to meet the regulatory requirements. SCA currently only applies to transactions where both your business’s bank and your customer’s bank are in the EEA or UK.

You can find out more about authentication requirements in our SCA compliance guide.

.avif)