Tokenization is playing an increasingly important role in the global effort to combat online payments fraud, and with great success.

According to Visa, the 4 billion network tokens it has issued to date have resulted in a 28% reduction in fraud rates and a 3% increase in approvals.

As ecommerce comes to account for an ever larger proportion of our overall commercial activity, tokenization becomes the cornerstone of a robust strategy to accept payments online. Tokenization is vital to protecting businesses and consumers, fostering trust, and maintaining the integrity of the global online payments ecosystem.

But what exactly is it?

In broad terms, tokenization is the process of replacing data — ordinarily the primary account number (PAN) — with something else, known as the ‘token.’ At some point later, the token is used as a key to unlock the data. The token is ‘housed’ in a different environment to the original data, and operates completely independently of it. Therefore the token cannot be used to hack into the data. In this way, tokenization is different to encryption, which merely scrambles data where it resides, and decrypts it when required. As such, the underlying data is vulnerable to hackers or corruption.

In this article, we explain how tokenization works, its role in fraud prevention, and the benefits of tokenization.

What is tokenization?

Payment tokenization is a security process that transforms sensitive card details, such as the Primary Account Number (PAN), into a unique and randomized sequence known as a token. The characters used for this token have no relationship to the original data, meaning it can’t be decrypted by a fraudster. Even if stolen, the token has no inherent value.

In the tokenization system, the association between the token and the cardholder data is securely maintained within a database referred to as a token vault. This vault is protected with encryption measures to safeguard its contents. When a customer initiates a payment, the token is transmitted through the payment network instead of any exploitable card details.

Why is tokenization important for fraud prevention?

Tokenization is important for fraud prevention because it replaces sensitive information that could otherwise be used to commit financial crimes with unique tokens that hold no intrinsic value. This means that, even if a token is intercepted during a transaction or a database containing tokens is breached, the stolen data is essentially useless to hackers since they cannot reverse-engineer the tokens to obtain the original data.

Additionally, implementing tokenization can help merchants comply with industry regulations that are designed to prevent fraud, including PCI DSS, and reduce the administrative burden of doing so.

Examples of tokenization used for fraud

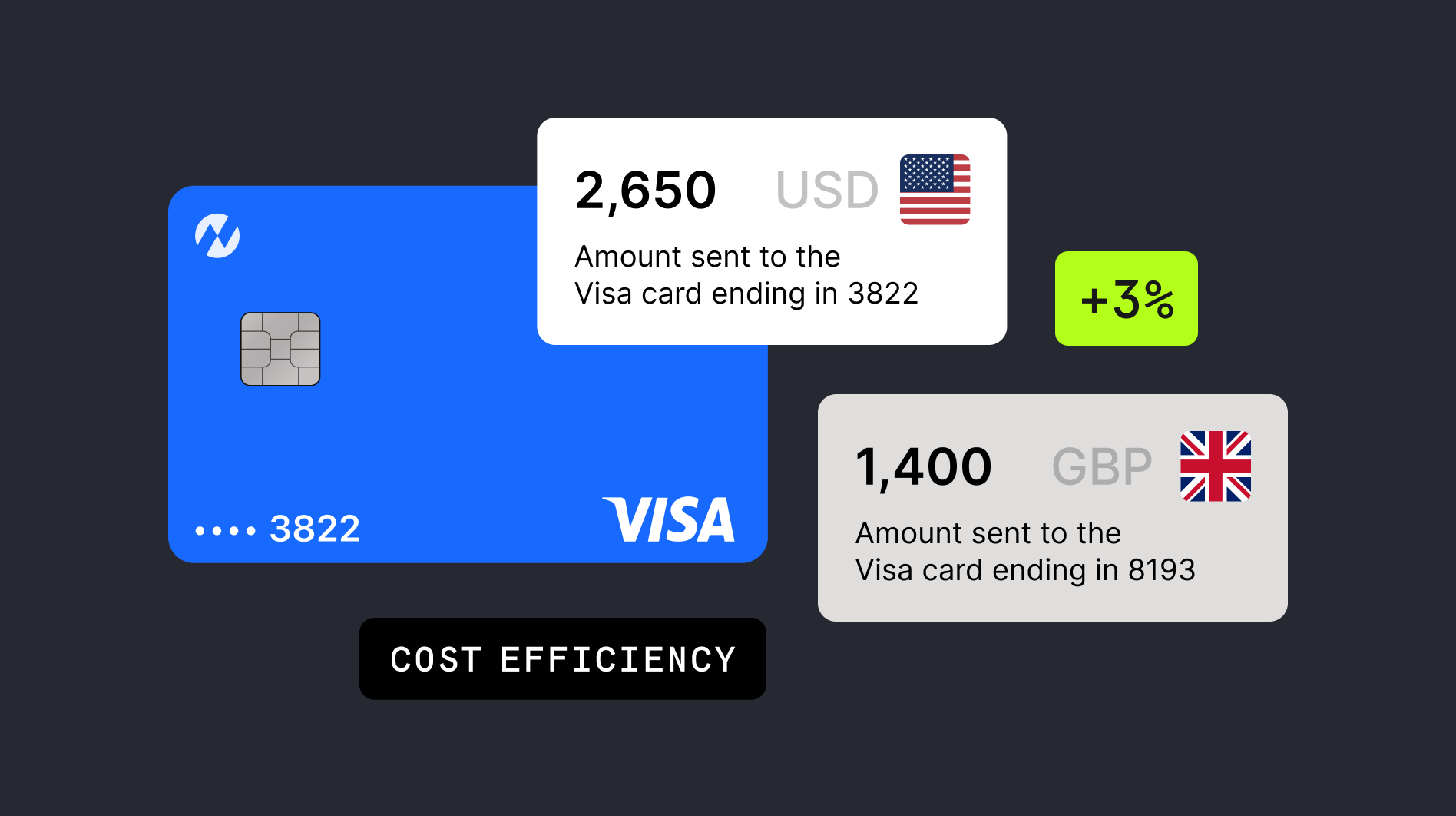

Total retail ecommerce sales increased from $1.3 trillion in 2014 to $4.2 trillion in 2021, and are expected to rocket to $81 trillion by 2026. At the same time, 2022 saw ecommerce payment fraud losses equal the total value of the ecommerce fraud detection and prevention market ($48bn).

The fight is on, and tokenization is on the frontline, protecting sensitive data from fraudsters throughout the transaction lifecycle. Network tokenization replaces the PAN across the entire payment ecosystem, meaning that the token is meaningful and interoperable across every player involved in the payment process.

This makes it a very useful tool for protecting card and digital wallet payments from fraud. When a customer makes a first purchase with a business, or when they add a new card to their digital wallet, the card information is captured and stored in a ‘token vault’. For future transactions, the token acts as the authorization for the business to take the payment, while keeping the data safe from fraudsters.

At the same time, tokenization helps businesses reduce their compliance burden for anti-fraud security standards like PCI DSS. It does this by limiting the amount of sensitive data they need to store, which minimizes the cost and resources required to safeguard the storage of that data from criminals.

For merchants, the great thing about tokenization as a fraud prevention measure is that it doesn’t have an impact on customer experience or the overall speed of processing a transaction. That means there’s no trade-off between keeping customers safe and keeping customers happy.

The benefits of payment card tokenization for fraud

1. Data security

Tokenization is a more secure technology than traditional encryption techniques because the card details are stored separately. Therefore a customer’s card details are not flying around the internet and payment networks, in danger of being hijacked. That makes data compliance easier, even more so if the business offloads management of the token vault to a third party.

2. Lower costs

Having more data compliance should equal less expense due to fewer risks to mitigate for and the absence of potential penalties. Also, tokenization does not have the pressure that comes with encryption of developing increasingly sophisticated (and costly) algorithms to ward off hackers.

3. Less payment friction

Security is not a business’s only concern. In truth, payment security has to be balanced with checkout convenience. Here’s where businesses can reap more benefits from tokenization. Whereas most security measures add friction, payment tokenization has relatively little, if any, negative impact on a customer’s payment experience.

4. False declines

False declines occur when legitimate transactions are mistakenly rejected due to suspicion of fraud. Tokenization helps to reduce these false declines in a number of ways.

Firstly, as it reduces the overall risk of fraud, fraud detection systems are less likely to find it necessary to block a tokenized transaction. Secondly, having built a database of essentially risk-free tokens for well-known or recurring customers, payments made using these ‘cards-on-file’ can safely bypass overzealous anti-fraud measures that can result in false declines.

5. Repeat purchases

Customers who make regular payments are likely to become frustrated if they need to input their card details every time they buy from you. Worse still if these are recurring payments—think subscriptions, installments, or utility bills—where customers like to ‘set and forget’.

With tokenization, businesses give customers what they want by enabling one-click payments or giving them the option to authorize future payments.

Learn more: What is push provisioning?

How Checkout.com enables tokenization

Checkout.com enables businesses to leverage payment tokenization by providing the software to generate PCI tokens. We are also able to embed PCI tokenization into your wider payments strategy. This is possible because Checkout.com also processes payments; in other words, we don’t need to hand over that aspect to a third party, with the extra risks and costs that come with that. By linking PCI tokenization with other core aspects of payments—such as checkout conversion, acceptance, and fraud—businesses create a more connected ecosystem, where opportunities are easier to identify and action.

To find out more, contact our team of payment experts.

.jpeg)

.png)

%20v1.jpg)

.png)