Transaction lifecycle

Last updated: March 4, 2026

A transaction is a collection of actions performed with an issued card. The actions are represented by individual messages such as authorization, reversal, clearing, and dispute. These messages define the transaction lifecycle.

During its lifecycle, a transaction transitions through various stages from initiation to completion, depending on the actions taken by the cardholder, merchant, issuer, and card scheme.

A successful transaction typically transitions through the authorization, clearing, and settlement stages.

In the European Union (EU), transactions are processed using the card scheme's dual message system, as follows:

- The merchant sends an authorization message to instantly verify and hold the funds in the cardholder's account.

- After the funds are verified, the merchant sends a clearing message at a later point in time to debit or credit the cardholder.

For example, when a cardholder makes an online purchase:

- The merchant sends the authorization message with the purchase details to the issuer for approval.

- After the merchant ships the items, the acquirer sends the first presentment message to the issuer to initiate clearing stage, where the merchant finalizes the transaction by requesting to capture the funds.

- In the settlement stage, the funds are transferred from the issuer to the merchant.

You can monitor changes in a transaction's status as follows:

- Configure your webhook server and subscribe to Issuing webhooks.

- Use the Transactions API.

Authorization is the initial stage of a transaction, which is used to confirm the following:

- The card and cardholder are genuine.

- The cardholder has sufficient funds to complete the transaction.

- The transaction is not restricted.

The merchant sends the issuer authorization requests in near real time, and Checkout.com typically responds within one second.

If you’ve enabled the authorization relay service, authorization requests are relayed to you so that you can approve or decline them.

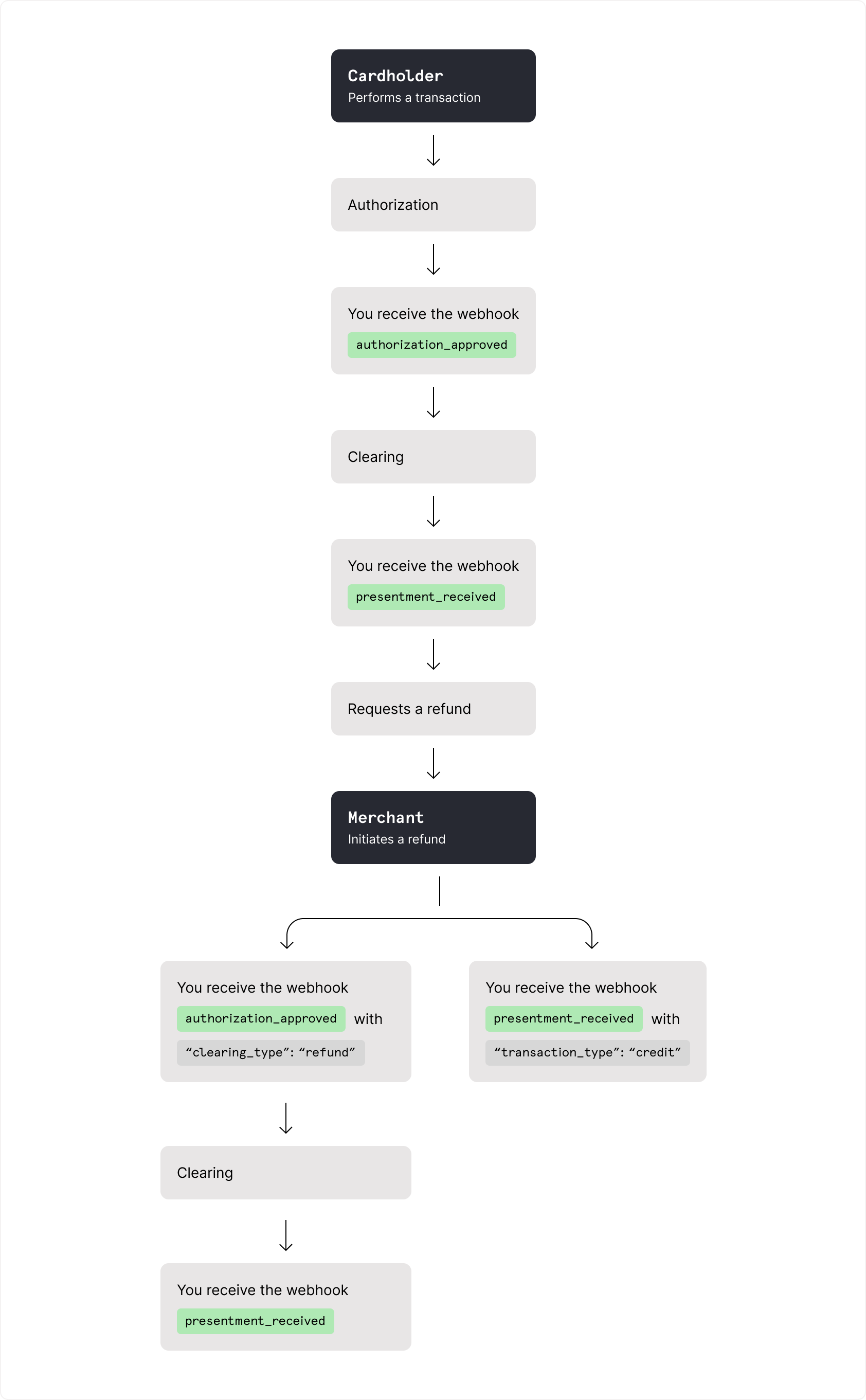

Clearing is also referred to as first presentment. A transaction enters the clearing stage when the merchant submits a capture request to finalize the hold on the funds and post the transaction on the cardholder's account.

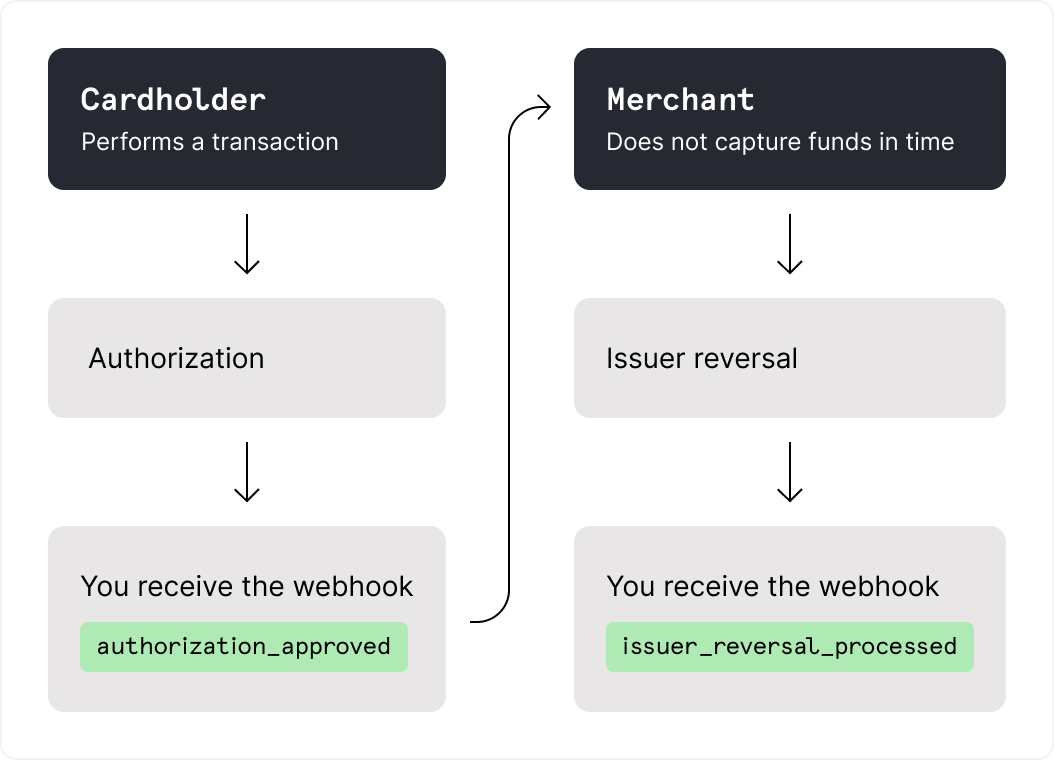

The merchant may request to only capture part of the initial authorization amount, known as partial capture. The remaining amount can be captured in a subsequent capture request or canceled. If no action is taken, the hold expires.

Clearing messages contain additional information about the transaction. For example, reconciliation amounts, interchange fees, acquirer fees, and cardholder billing amounts. The card scheme uses this information to calculate the final amounts to be settled.

Information

The reconciliation amount is the amount settled with the card scheme, excluding interchange fees or any other fees. This amount is represented in the issuer's settlement currency.

When clearing is completed, the transaction enters the settlement stage, where the funds are transferred from the issuer to the merchant.

The card scheme runs five daily settlements. Checkout.com provides this information to you in reports. If you use shared BINs, we report this per cardholder.

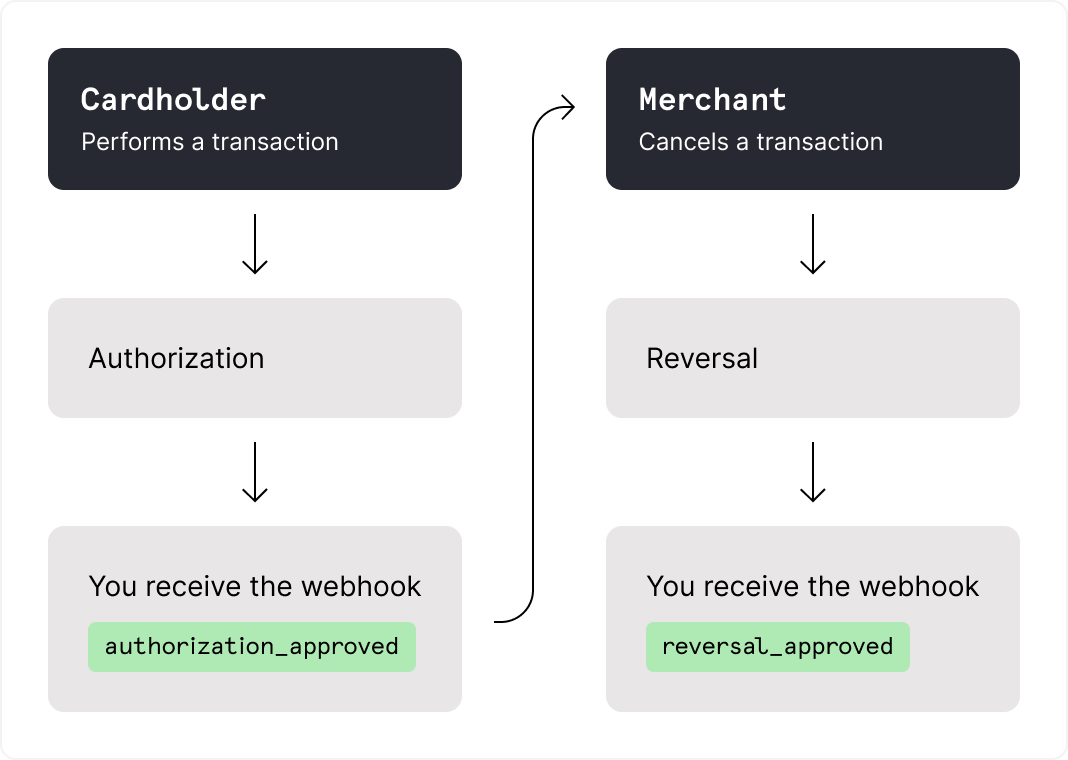

Reversal is the process of canceling or updating a previous authorization before the payment enters the clearing stage. This stage can be initiated by either the merchant or the issuer.

A merchant reversal occurs when the merchant cancels the transaction after a successful authorization, but before it enters clearing.

The merchant may also choose to only reverse part of the initial authorization amount, known as a partial reversal. The remainder can then be captured in a partial capture request from the acquirer and enter clearing.

A refund occurs when the cardholder requests that the merchant returns the funds from a transaction after clearing is complete.

A refund can either be included in the transaction's clearing information, or be preceded by a refund authorization request that the issuer can approve or decline.

A chargeback occurs when the issuer disputes a completed transaction on behalf of the cardholder. It can be for the full amount that was cleared or a partial amount, and is sent to the merchant.

In some cases, the issuer can reverse a chargeback. For example, the cardholder accepts liability for the dispute after the chargeback is initiated but before the acquirer responds.

Information

For more information, see Manage Issuing disputes.