Visa’s rules around fraud and disputes are changing. Visa retired its previous monitoring programs for disputes and fraud on April 1, 2025, and launched a new, combined dispute and fraud program: the Visa Acquirer Monitoring Program (VAMP).

Previously, Visa had five different systems for managing fraud and disputes, including the Visa Fraud Monitoring Program (VFMP) and the Visa Dispute Monitoring Program (VDMP). Now, VAMP has taken their place.

You need to know about VAMP to avoid any additional fees. This blog post breaks down the key information, so you can get it right.

Remember, the lower your fraud rates, the more confidence issuers will have in your payment traffic. As you gain a better reputation as a merchant that sends good quality payments through, you could see improved acceptance rates over time. Reason being, issuers are more likely to accept payment requests from a merchant which sends very low volumes of payments flagged as fraudulent.

What is the Visa Acquirer Monitoring Program (VAMP)?

VAMP is the new way in which Visa will assess fraud and dispute rates in payments. It replaces Visa’s various existing fraud and dispute programs – as well as 38 distinct remediation processes – and introduces updated thresholds.

Visa said its program aims to create clarity and consistency for acquirers and their merchants by creating globally aligned fraud thresholds for both domestic and cross-border card-not-present transactions. Overall, VAMP is part of Visa’s efforts to reduce the prevalence of fraud and disputed transactions. There are two main parts: a ratio calculation and an “enumeration” part. You only qualify for the threshold if you reach a certain count (volume) of disputed transactions and fraud per month. In addition, the enumeration aspect takes into account how many times a card is tried and how often these attempts fail, so merchants can spot and stop fraudsters who keep trying different card details to guess the right ones.

We have published an update to the Visa Acquirer Monitoring Program with the latest acquirer and merchant ratios for disputes and fraud. There have been a number of changes to this program in the first half of the year, so it’s worth checking on our VAMP Documentation and reading all emails from us to stay updated.

How does the VAMP Ratio calculation work?

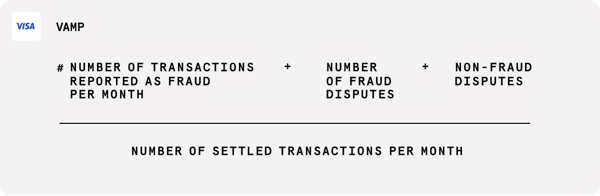

Specifically, the VAMP calculation is based on fraud (TC40) and dispute (TC15) rates for card-not-present transactions.

The minimum count for identification is now 1,500 monthly (TC40 fraud and TC15 disputes). Because of this, only merchants with enough transaction volume could potentially face fines under the new rules.

Merchants and acquirers must keep their fraud and disputes below a certain ratio – or face fees. This is the important formula, known as the VAMP Ratio:

Here’s what isn’t included, according to Visa:

• Excludes (TC15) disputes resolved through pre-dispute solutions, contingent on the timing of the data extract.

• Excludes (TC40) fraud transactions qualified for Compelling Evidence 3.0, contingent on the timing of the data extract.

Solve payment disputes quickly

It’s important to aim to resolve a TC40 or TC15 dispute within the same month it was raised. Otherwise, the disputes will be counted in your VAMP ratio. We’ll cover Visa-backed solutions to reduce your payment disputes, further below.

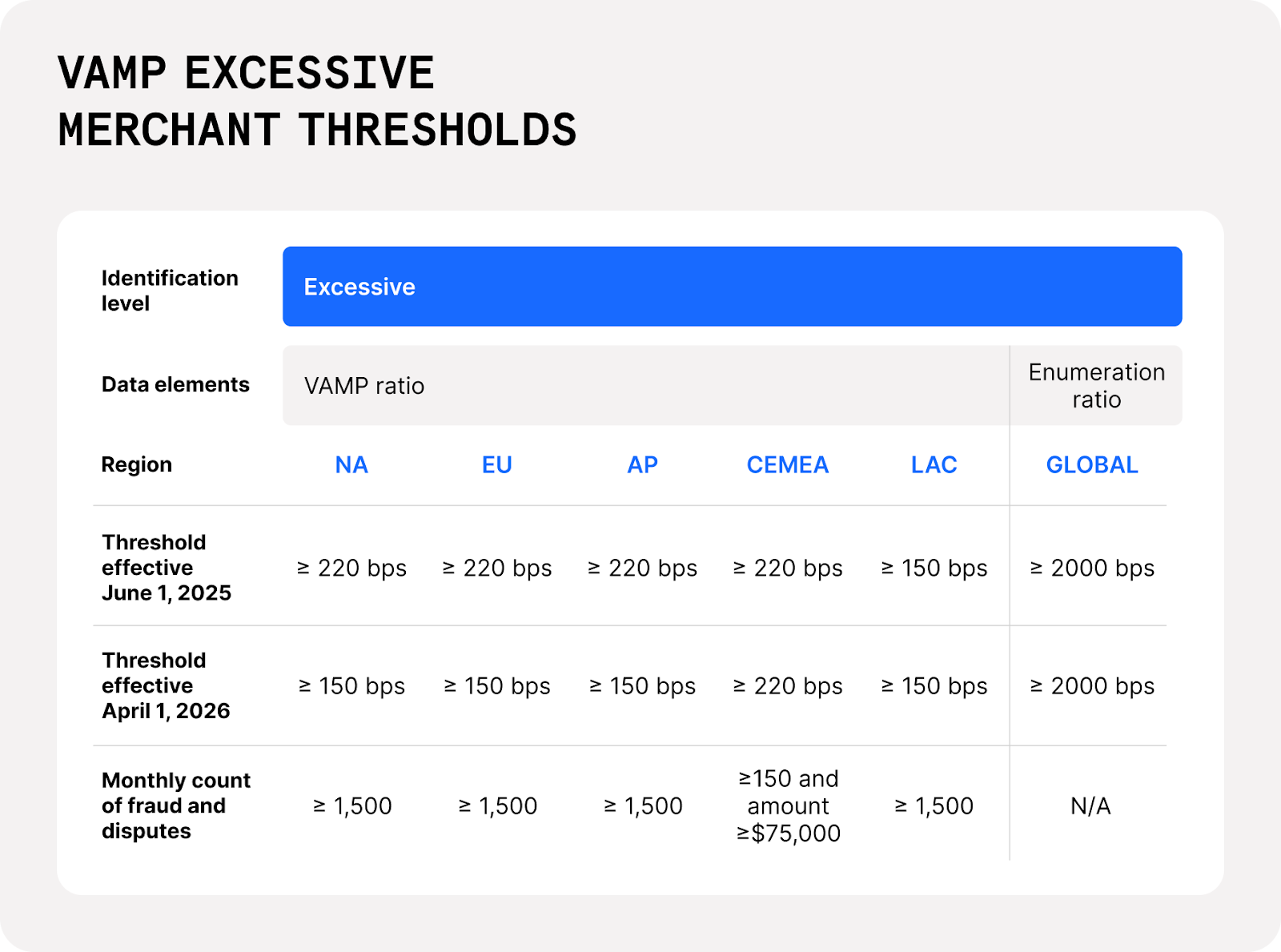

Summary of VAMP Ratio thresholds

It’s now common practice to track VAMP thresholds by basis points (BPS), as Visa sets out in its official guidance:

What are the VAMP enumeration rules?

Visa’s excessive enumeration ratio applies to enumeration attacks (i.e. automated card testing fraud) identified by Visa’s machine learning model, the Visa Account Attack Intelligence system.

If you have more than 300,000 Visa-identified enumeration attacks in a month that are more than or equal to 20% of your transaction volume, you’ll fall under the excessive enumeration program.

Note: At the time of writing, Visa said it will not assess fines for merchants that breach the ‘Excessive’ threshold under the VAMP Enumeration Ratios. Monitor the latest updates from Checkout.com to see if this changes.

When does VAMP come into effect?

VAMP is already active, and merchants in the excessive category began to be identified at the beginning of the four-month Visa ‘Advisory Period’ which began in June. Potential fines for excessive merchants begin from October 1, 2025. These will apply to transactions from the previous month, of course, meaning merchants need to carefully monitor their fraud and disputes ratios in September or risk fines in October.

Lower thresholds will apply globally (excluding the Middle East and North Africa) from April 1, 2026.

What is the difference between the VAMP and the old system?

All merchants must be careful to check they understand the rules of VAMP.

The old systems were value-based, and VAMP is volume-based. Broadly speaking, this prompts a change in the kind of merchants that the rules particularly correspond to; the old system would more often relate to low volume, high value transactions. Now, VAMP will be of even greater importance to merchants with higher transaction volume, such as large retailers, marketplaces, discount stores, mobile gaming merchants, and fintechs.

VAMP itself has also undergone numerous changes since its initial launch. One of the biggest changes is the calculation: previously, Visa only included non-fraud disputes in the disputes ratio. Now, fraud disputes and transactions flagged as fraudulent are also included.

What to do under the new VAMP rules

It’s now more important than ever to monitor the total number of payment disputes coming through your business, as well as staying on top of fraud as a whole. Enumeration attacks are penalized under VAMP, so it’s additionally vital to take measures that defend against card testing fraud.

At the same time, you want to minimize false positives and let legitimate transactions through. This will ensure you can continue to provide a great experience to your customers, and keep revenue running smoothly. For that reason, you need a finely-tuned fraud strategy that takes into account your specific business model, payment patterns, and customer habits. Our Fraud Detection solution combines custom rules with machine learning to help you achieve this critical balance.

With the new changes now in effect, it’s important you have the right tools and support to ensure you avoid undue penalties. When it comes to payment disputes, there are a number of fees, including additional costs passed on from the card networks. We understand it’s not generally practical to manually investigate every single payment dispute that arises. However, you need to pay close attention to the number of fraud claims and disputes raised on your payments, as these can lead to chargebacks, which negatively impact your bottom line as well as your customer satisfaction.

Reduce VAMP ratio with Visa-backed solutions

There are a few Visa-approved ways to help stay on the right side of VAMP:

- Visa Compelling Evidence 3.0, which helps provide proof of prior legitimate purchases to demonstrate a customer legitimately made a payment.

- Chargeback Dispute Resolution Network (CDRN) provided by Verifi, a Visa solution which helps to resolve fraud and non-fraud disputes and prevent chargebacks.

- Ethoca, which provides coverage of the MasterCard network, can also be used to reduce the number of payment disputes and chargebacks.

- Rapid Dispute Resolution can help keep costs down by triggering a refund to the customer on selected disputes. It has cut down the sales-to-chargeback ratio for our merchants by 58%, as well as saving the time and effort of human review.

These solutions can be particularly helpful as they involve a level of automation for the dispute-handling workload. Importantly, transactions resolved through any of these listed methods are exempt from the VAMP calculation.

Dispute and fraud support from Checkout.com

Overall, VAMP is a reminder to consider ways to bring down the number of payment disputes and payments flagged as fraudulent, particularly in the case of first-party or friendly fraud.

Our team is here to help you get it right. We offer VAMP ratio monitoring and proactive alerts to help you stay ahead of threats. Your account manager will contact you if your merchant account is at risk of being placed under the VAMP, and let you know the next best steps.

If you are interested in taking extra measures to prevent excessive ratios, you can look into our Fraud Detection, and contact us to find out more. Our Risk SDKs and API data capture provides enhanced signal collection to boost fraud model accuracy, so you can confidently manage your fraud risks.

In terms of acquirer ratios, we carefully monitor our fraud and disputed transactions flows to ensure we stay on the right side of all scheme guidelines, including VAMP.

%20(1).png)

.png)