Set up card program

Last updated: October 22, 2025

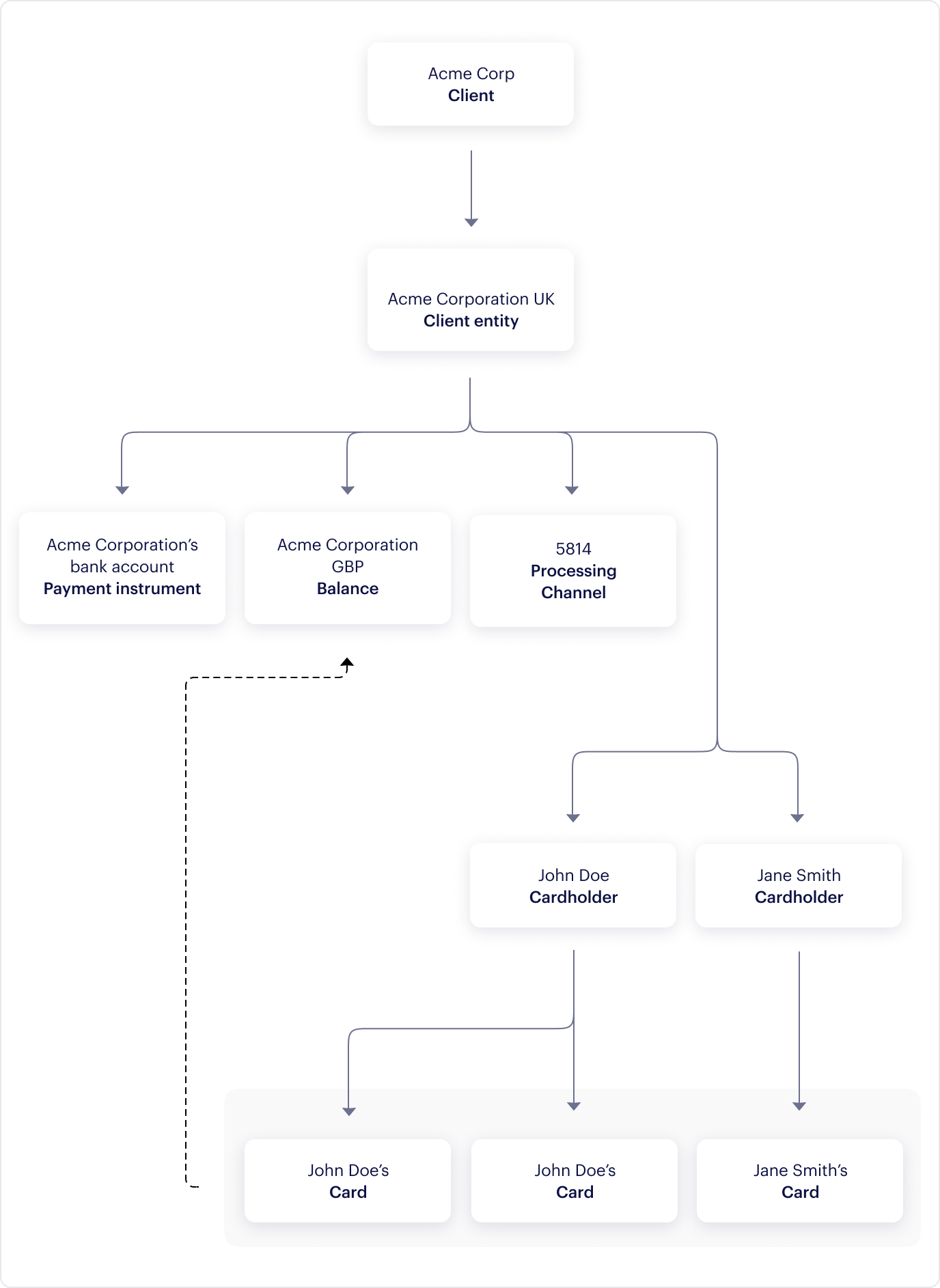

To issue cards, you must first set up a card program with Checkout.com. A card program is a payments product that enables you or your customers to make card payments to suppliers or merchants, anywhere in the world.

To understand your card program requirements, Checkout.com sends you a questionnaire during your Issuing onboarding. It asks you to provide the following information about your business:

- Operational setup – including fraud, risk, compliance, finance, and customer-service information

- Transactional volumes and limits – including average transaction value (ATV), daily and monthly limits, and merchant category code (MCC) restrictions

- Policies and procedures – including anti-money laundering (AML), anti-bribery, counter-terrorist financing (CTF) measures, and Know Your Customer (KYC) checks

Checkout.com uses the information collected from your answers to inform:

- Your issuing account setup

- The characteristics of the card product(s) you require based on your needs

Your account setup depends on your use case, and the answers you provided in the onboarding questionnaire. Among other things, your setup determines the relationship between:

- Checkout.com

- Your business entity

- Your cardholders

- How you fund your Issuing balance

You are a processing-only client if both of the following are true:

- You are licensed as an issuer with card schemes and manage the flow of funds.

- You use Checkout.com to process Issuing transactions, but not to issue cards.

Checkout.com can issue cards to individuals within your business. For example, to make payments to your suppliers or partners.

You can also issue cards directly to your individual customers.

A card product is a unique configuration of card characteristics, including:

- The card scheme – Mastercard, or Visa (beta)

- The issuing country and currency

- Whether the card is commercial or consumer

- Whether the card is debit or prepaid

- Whether you can issue physical cards, virtual cards, or both

- Shipping options for physical cards

- Whether the card is single or multi-use

- The card's lifetime

- 3D Secure (3DS) settings

When you issue a card and specify the card product ID, the card automatically inherits the card product's characteristics.

Card products are configured at entity level, and each entity can have more than one card product. For example, an entity that operates across multiple regions may need a card product for each issuing country and currency they require, while the other card characteristics remain the same.

You can issue cards throughout the European Economic Area (EEA) and in the UK.

You can issue cards in the following currencies, depending on the Checkout.com entity you are contracted with:

EUR– EuroGBP– Pound SterlingUSD– US Dollar

A commercial card is issued to your own business. For example, to pay suppliers. A consumer card is issued to your customers to make payments.

The information you need to provide to Checkout.com depends on whether the card product is for a commercial or consumer use case:

| Card information | Commercial cards | Consumer cards |

|---|---|---|

Country and currency of the card | Required | Required |

Loading mechanisms for the card | Required | Required |

Whether the card is debit or prepaid | Required | Required |

Whether the card can be physical, virtual, or both | Required | Required |

Transaction volumes | Required | Required |

Card spending limits | Required | Required |

Card controls | Required | Required |

Whether the card is accessible using ATMs | Required | Required |

Whether Apple Pay and Google Pay are enabled for the card | Required | Required |

How you source and onboard your customers | Not required | Required |

How you operate your card program in terms of customer service, fraud management, and AML processes | Not required | Required |

Any fees charged for the card | Not required | Required |

A prepaid card is preloaded with funds that are available to the cardholder. To issue prepaid cards, you must have a prepaid business identification number (BIN).

You can configure the card to be:

Prepaid cards have the following limitations:

- Cashback is not available.

- The maximum daily load limit is 5,000 USD.

A debit card enables cardholders to access funds from your Issuing account balance. You can also link debit cards to an e-money account where your customers' funds are held.

Debit cards are typically more widely accepted than prepaid cards, and support cashback.

To issue debit cards, you must meet the following requirements:

You must:

- Have a debit business identification number (BIN).

- Provide a live customer-service channel – for example, phone or live chat. Email support is not sufficient.

- Issue a physical card associated with the account.

- Perform full Know Your Customer (KYC) and Know Your Business (KYB) checks on cardholders. Anonymous cards and simplified due diligence are not accepted.

Cardholders must be able to:

- Load the e-money account by wire transfer - for example, through SEPA, Faster Payments, or Swift.

- Access their balance and transaction history through the internet, ATMs, a call center, and interactive voice response.

Cards must:

- Have global ATM access.

- Support purchases with cashback transactions.

Physical cards enable your cardholders to make payments both online and at physical points-of-sale (POS), and withdraw cash at ATMs.

The card is shipped to the cardholder, along with the personal identification number (PIN). Alternatively, if you integrate the Android or iOS Card Management SDK, the cardholder can view the PIN in your mobile app.

Physical cards must be activated before the cardholder can make payments. You can configure to activate them on creation, or activate them later.

Virtual cards enable your cardholders to make payments online only. No shipping or PIN is required.

Cards must be activated before the cardholder can make payments. You can configure to activate them on creation, or activate them later.

Single-use cards are automatically revoked after one successful transaction. Multi-use cards are usable until all funds are spent.

For reloadable cards, you can add more funds when the initial balance has been spent. For non-reloadable cards, once the initial balance is spent, you cannot add more funds.

- Sign in to the Dashboard.

- Go to Issuing > Card program.

- On the Card products tab, you can view the following for each card product:

- Name

- Currency

- Card product ID

- Scheme

- Cards created

- Date created

- Sign in to the Dashboard.

- Go to Issuing > Card program > Card products.

- To download all card product details as a CSV file, select Export.

- To download the details of specific card products, you can filter by currency or issuing country, or search by card product ID.

Then, select Export to download the filtered results as a CSV file.