When money moves, value is created – or lost. Customers increasingly expect fast access to funds, timely payouts, and the ability to use their money when they need it, from insurance settlements to salaries and cross-border remittances.

At the same time, CFOs expect payment costs to fall as transaction volumes grow.

That’s where Checkout.com comes in. Checkout.com’s new five-year collaboration with Visa Direct strengthens how enterprises move money across multiple markets. Through this collaboration, merchants are able to support faster settlements and improved customer experience.

“This collaboration helps unlocks new possibilities for cross-border money movement use cases and builds on years of trust and impact. Together with Visa, we’re helping our merchants scale faster, operate smarter, and thrive in a competitive ecosystem,” shares Matthieu Barral, Global Head of Financial Partnerships at Checkout.com.

This article explores:

- Two commonly used Visa Direct transaction types – Account Funding Transactions (AFTs) and Original Credit Transactions (OCTs)

- How different industries use these transaction types to improve customer experience

- Why processing Visa Direct transactions with Checkout.com can help deliver cost efficiencies

Vira Platonova, Global Head of Visa Direct comments: “Visa Direct is expanding what's possible in global money movement, and Checkout.com has played an important role in bringing innovative use cases to market. Together, we’re empowering businesses to deliver faster, smoother fund flows that meet the expectations of today’s digital economy.”

Understanding the building blocks of Visa Direct: AFTs and OCTs

At its core, Visa Direct is a money movement network that supports fast push-to-card, wallet, and account payouts across billions of eligible cards and other supported endpoints within the Visa ecosystem. Today, Visa Direct enables transactions across 195+ countries and territories and more than 150 currencies.

Card payouts using Visa Direct differ from traditional bank payouts which are often used for periodic transactions with fixed schedules. With the fast and broad reach supported by Visa Direct, card payouts can help improve customer satisfaction and business outcomes, particularly for fast-paced, high-volume payment environments.

Businesses can potentially uncover new commerce corridors while managing FX through Checkout.com’s capabilities, including access to up-to-date FX rates and forward contracts.

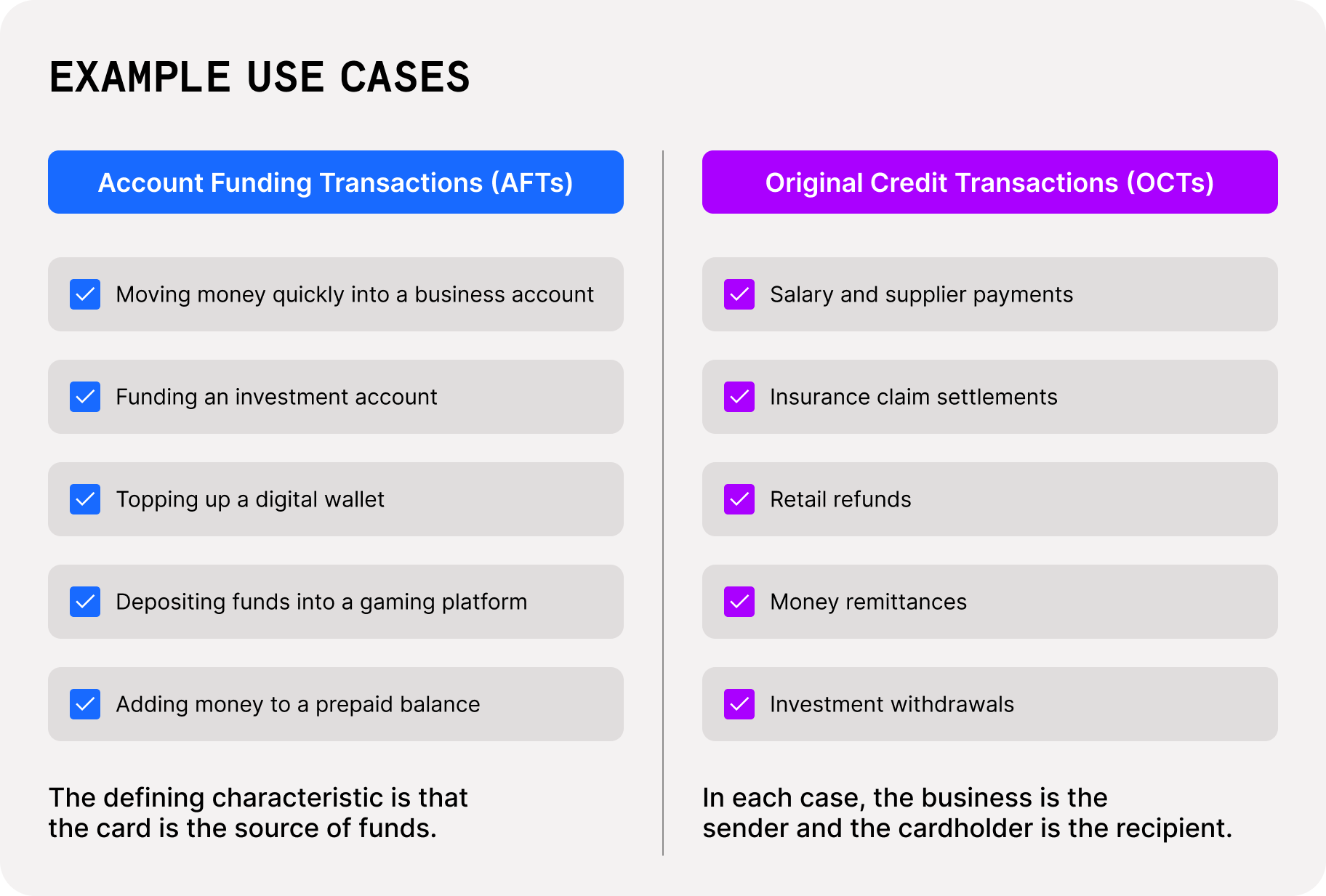

There are two primary transaction types: Account Funding Transactions (AFTs) and Original Credit Transactions (OCTs). While both use the same network, they serve different strategic purposes.

Checkout.com provides merchants with access to Visa Direct capabilities through a single API integration, enabled via its acquiring and financial institution partnerships, where available.

Want to know more about Visa Direct and how it works? Read more here.

1. Account Funding Transactions (AFTs)

An AFT helps facilitate the movement of money from a customer’s debit or credit card to a prepaid card, digital wallet, investment account or other stored-value account. In simple terms, it’s a card-funded top-up – for example, adding $50 to PayPal account from a Visa card.

Why AFTs matter:

AFTs help facilitate fast account funding from cards to stored-value accounts. For businesses operating in time-sensitive environments – such as trading platforms, digital asset platforms, and gaming operators – faster funding can help support higher engagement and revenue opportunities.

When customers can fund quickly, they’re able to take action sooner.

2. Original Credit Transactions (OCTs)

An OCT helps facilitate the movement of money from a business to a customer’s eligible card. Instead of initiating a traditional bank transfer, the business pushes funds to the recipient’s card, where they can often access the money in minutes, depending on the receiving financial institution and region.

Why OCTs matter:

OCTs can support real-time or fast card-based disbursements, providing an alternative to traditional payout methods. Rather than relying solely on bank transfers, recipients may be able to access funds more quickly, depending on the receiving financial institution or market availability.

For enterprises, faster disbursements can help improve customer satisfaction, reduce support inquiries, and support greater working capital flexibility.

Disclaimer: Actual fund availability for all Visa Direct transactions may depend on receiving financial institution, account type, region, compliance processes, along with other factors, as applicable.

Together, AFTs and OCTs create a two-way, card-based money movement loop. Customers can fund accounts more quickly, and businesses can disburse funds efficiently – helping improve both customer experience and operational efficiency.

Taking a vertical view: How Visa Direct supports impact across industries

While AFTs and OCTs work similarly, the strategic impact of Visa Direct varies by industry. The question goes beyond speed alone: how can faster money movement support customer experience and revenue?

Here’s how that plays out across key verticals.

Insurance: Transforming claims into loyalty moments

Insurance claims are often emotionally charged moments. Speed of payout has a direct impact on customer trust. Traditional bank transfers can take days, creating uncertainty at precisely the moment reassurance is needed.

With OCTs, insurers can push claim settlements or emergency disbursements directly to a policyholder’s eligible card, enabling faster access to funds, where available. Faster payouts can help improve customer satisfaction and may reduce inbound queries, easing the operational burden on your business.

As Wayne Slavin, CEO of Sure, Inc. shared in our Trust in the Digital Economy report “One of the most significant barriers to digital transformation in insurance lies in its outdated payment infrastructure. [...] Addressing these challenges requires the adoption of integrated, real-time payment solutions.”

Wayne continued, “Our research highlights that 44% of consumers consider claim payout speed to be ‘very important’, yet only 25% express satisfaction with current claims processing times. [...] We know that when it comes to any receipt of funds for consumers, speed and transparency are critical factors in consumer trust and loyalty.”

By complementing traditional bank transfers with Visa Direct, insurers can use faster payouts as a way to stand out and transform claims from high-stress moments into loyalty drivers.

Investment and trading platforms: Funding at market speed

For trading and investment platforms, timing is everything. It directly impacts revenue. Slow funding can mean missed opportunities or abandoned transactions.

AFTs via Visa Direct allow customers to fund brokerage accounts, ISAs, or digital asset platforms using their cards, which can support faster access to funds where available.

On the other side of the lifecycle, OCTs can support faster withdrawals back to a customer’s eligible card. Faster access to funds can build trust, reduce churn, and reinforce platform credibility.

When markets move in seconds, relying on slow or unpredictable funding and withdrawal timelines can be a pain point for both platforms and customers.

Remittances: Creating speed and reliability across borders

Cross-border remittances require reach and reliability, as delays can affect recipients’ essential needs. Visa Direct is useful for remittance platforms covering funding and payments across different geographies and currencies.

Using OCTs to push funds directly to eligible cards can reduce dependence on cash pickups or traditional bank rails. It also enhances traceability and simplifies operational processes, lowering overheads.

For providers, card-based payouts can offer a compelling combination of speed and operational reliability, helping customers to send money to family and friends abroad with greater convenience.

Gig economy and payroll: Redefining pay cycles

Today’s workforce increasingly expects flexibility, with gig workers like ride-share drivers, food delivery couriers, and freelance marketplace sellers often needing access to earnings on demand. When your next paycheck isn’t guaranteed, quick access to earnings carries even more weight.

Visa Direct enables platforms to push earnings directly to workers’ eligible cards using OCTs, supporting faster access to funds where available.

Early wage access (EWA) providers can use card‑based payouts enabled by Visa Direct to help modernize payroll experiences without requiring an overhaul of core banking infrastructure, typically allowing workers to access a portion of their wages or earnings.

The above factors contribute to simplified reconciliation, while creating happier workers and helping generate stronger platform growth.

Ecommerce and retail: Accelerating refunds

The speed of a refund can make or break customer loyalty. Today’s shoppers equate refund speed with brand credibility. Over half (54%) of US consumers expect a refund within 24 hours, and 67% say a poor return experience would discourage repeat shopping. Fast options also influence choice, with 71% preferring immediate refunds or exchanges.

Visa Direct OCTs can accelerate card refunds, so retailers can shorten the time between approval and when funds are sent to the customer’s eligible card. That not only improves customer satisfaction but can also reduce call center volumes and operational overhead.

Fast, accurate refund capabilities can help manage the complexity of limited reconciliation systems, treasury workflows, and fraud controls more efficiently. They can also help protect the business by reducing the risk of disputes from customers wondering where their refund is.

Quick refunds are especially valuable during peak seasons, freeing working capital and improving cash flow visibility.

Even if a customer’s purchase didn’t work out, it’s still important to keep them wanting more.

Read more about the importance of fast refunds.

Why process Visa Direct with Checkout.com?

Checkout.com’s collaboration with Visa Direct introduces an additional dimension beyond speed and scale: cost efficiency tied directly to growth.

“By integrating Visa Direct's global network with our high-performance platform, which abstracts payments technology and regulation into a single global solution, we’re providing merchants with fast, reliable access to card-based payouts across an unprecedented range of currencies, markets, and use cases,” adds Avishkar Sharma, Head of Commercial Financial Partnerships at Checkout.com.

1. A structural cost advantage that scales with volume

Through this strategic partnership, Checkout.com supports scalable Visa Direct processing that can help merchants manage costs as volumes grow, subject to market availability and commercial terms.

For large enterprises, this changes the equation. Payouts and funding flows are often seen as unavoidable cost centers. Under a volume-linked incentive model, they become an opportunity to drive down business costs as activity scales. The more traffic centralized through Checkout.com, the greater the potential economic benefit.

2. Centralized pay-ins and payouts in one Business Account

Operational fragmentation is expensive.

By consolidating payins and payouts in one Checkout.com Business Account, merchants may be able to use the funds from accepted payments to support certain Visa Direct payouts flows, subject to configuration and commercial arrangements. This approach can help reduce the need for separate prefunding steps or balance transfers between providers.

First and foremost, this can help boost speed because there’s no additional waiting time to top up the account. But beyond speed, that centralization can help payment teams streamline liquidity management, reconciliation processes, and improve working capital efficiency over time.

3. Performance-led payout infrastructure

Cost efficiency only works if transactions perform. And at Checkout.com, performance is our obsession. Our infrastructure is designed to optimize payout acceptance and reliability with a set of built-in features.

Key capabilities include:

“Fail fast” logic

We validate as much of the payment request as possible upfront and provide real-time error feedback. This way, merchants can fix data gaps immediately and only attempt payments with schemes they’re approved for.

Card metadata API

We use Account Number Control List (ACNL) files to check card eligibility before a request is fully processed to improve routing decisions.

Smart retries

We’re introducing behind-the-scenes soft decline reattempts to recover otherwise lost transactions without merchant intervention.

For high-volume enterprises, even small improvements in acceptance rates can translate into significant recovered revenue.

4. Enterprise-grade visibility and control

Operational visibility is another consideration for enterprise payments teams. Payments leaders need insights.

Checkout.com’s dashboard provides granular, real-time transaction data that gives merchants the insights needed to improve performance and scale, while dialing in the perfect level of control and flexibility. Having detailed reporting and control is as important as the underlying processing capability.

5. Extensive geographic coverage

Finally, geographic coverage matters. The ability to support card-based payouts from multiple major geographies through a single provider can reduce operational fragmentation and simplify expansion strategies.

Through its platform and participating financial institution relationships, Checkout.com supports push-to-card payouts capabilities using Visa Direct in select markets and configurations, including:

- United States

- United Kingdom

- European Economic Area (EEA)

- Singapore

- United Arab Emirates

Availability varies by transaction type, issuer participation and local regulatory requirements.

A partnership built for long-term growth: From faster payments to better cost efficiency

Visa Direct supports fast, card-based money movement across a broad range of countries and territories. The strategic partnership with Checkout.com adds a longer-term financial dimension: aligning transaction growth with cost efficiency.

The opportunity is twofold. First, deploy AFTs and OCTs to help enhance customer experience across funding, payouts, and refunds – supporting faster funding through AFTs and accelerated payouts with OCTs. Second, use volume consolidation and incentive structures to support operational efficiencies that can help drive down unit costs as volume scales.

In an environment where margin pressure is constant and customer expectations are rising, optimizing how money moves is essential.

“By combining Visa’s global network and reach with Checkout.com’s modern, AI-driven technology, we’re helping businesses improve payments performance and drive more efficient, reliable money movement at scale,” said Chris Newkirk, President, Commercial & Money Movement Solutions at Visa.

.png)

.avif)