_interchange%20revenue%20explained.png)

Interchange is a crucial part of the global card payments system. It allows everyone involved in the card transaction process to have a fair slice of the pie, and provides a stable and predictable source of revenue for card networks and issuing banks.

But there is no one interchange rate, and it can vary significantly depending on everything from what sector you operate in to where your business is based. But what do you actually need to know?

In this article, we’ll give you the interchange revenue definition, explain how it enables businesses to unlock new revenue, as well as what factors affect interchange fees, and tell you how you can maximize your interchange revenue.

What is interchange?

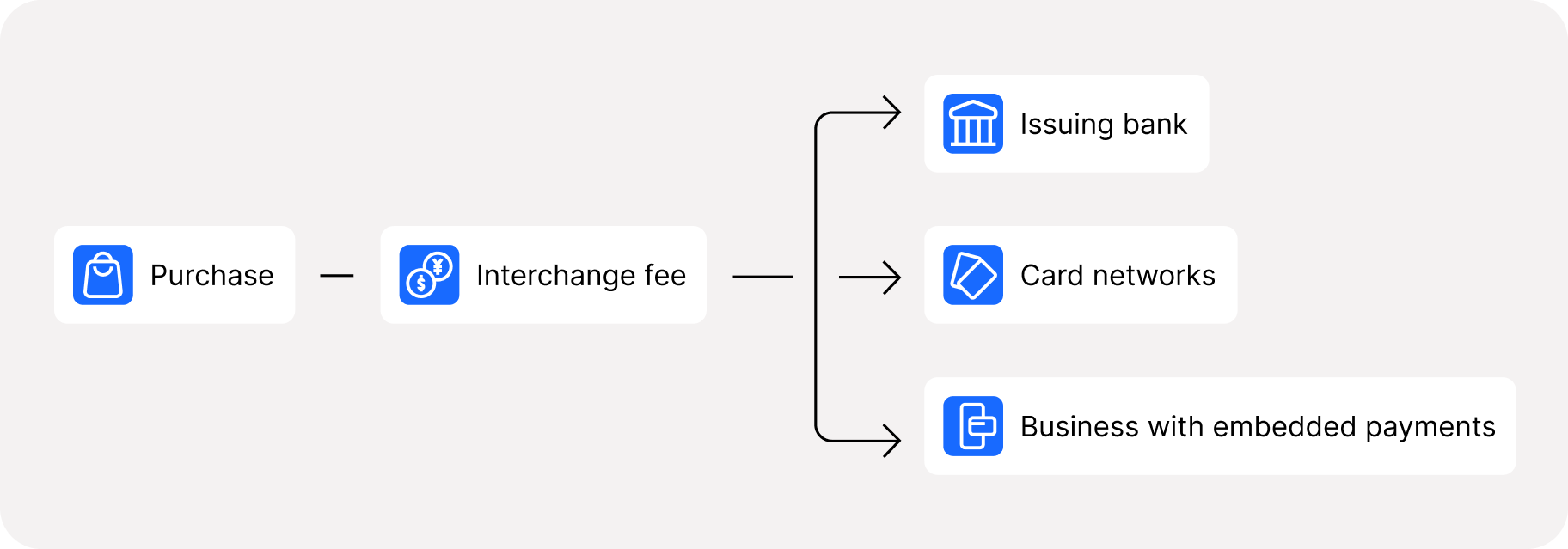

Interchange enables businesses to accept credit card payments by connecting them with the credit card networks and the issuing banks. When a customer uses their credit card to purchase goods or services, you’re charged an interchange fee by your credit card network. This fee - roughly between 1% and 3% of the transaction value - compensates the card network, the issuing bank, and any other party involved in the transaction for the costs associated with processing and settling the payment.

Essentially, the interchange fee helps to ensure that everybody involved in a credit card transaction is fairly remunerated for their services. So, for example, if the interchange rate is 1.5%, on a $50 purchase, the customer might spend $48.50 on the product, as well as 75 cents on processing fees, and another 75 cents that’s distributed between the network (bank and other parties).

In 2011, the Durbin Amendment was enacted in the US, which capped the interchange fees charged to merchants who accept debit card payments using debit cards issued by any bank with more than $10 billion in assets. The aim was to reduce what were deemed to be disproportionate and unfair fees passed onto consumers.

How does interchange work & enable businesses running their own card programs to unlock new revenue?

Card networks set the interchange fee, typically a percentage of the transaction value, plus a fixed amount. For each transaction this interchange fee is split between the different parties involved, including a share for the business that issued the card.

The amount of interchange revenue earned by the card issuer for each transaction is small on its own, but cumulatively, can add up to a huge amount.

Many businesses that issue card have been able to unlock a massive source of funds - aka interchange revenue - which allows them to maintain and improve their card program and tap into a wider customer base.

Read more: Revenue recognition explained

What factors affect interchange rate?

As we explained earlier, the interchange rate is generally between about 1% and 3% of the value of the transaction. It’s hard to say exactly how to calculate interchange revenue, because it can change so much depending on your circumstances.

The factors that dictate interchange rate include:

- Card type - different types of credit cards, such as consumer credit cards, business credit cards, rewards cards, and premium cards, have different interchange rates.

- Card network - likewise, the interchange rate varies depending on the credit card network. i.e. Visa, Mastercard, American Express.

- Transaction type - interchange rates can also vary depending on the type of transaction being processed, such as a card-present transaction (where the card is physically present) or a card-not-present transaction (an online or over-the-phone purchase).

- Merchant Category Code (MCC) - the MCC is a four-digit code assigned by the card network that identifies the type of business that is accepting the card. Certain MCCs, such as those for hotels, airlines, car rentals, and higher risk businesses, have higher interchange rates.

- Merchant size - the size of the merchant can also play a part, as larger companies are able to negotiate lower rates

- Security protocol - the more secure the transaction, the lower the fee.

- Country of transaction - interchange rates can vary depending on the country in which the transaction is being processed. European fees tend to be lower than those in Northern America.

- Country of issue - if the acquiring bank and the issuing bank are located in different countries, the payment process is more complicated, resulting in a higher interchange rate.

- Card issuing bank - issuing banks can negotiate their own interchange rates with card networks.

- Transaction amount - because fees consist of both fixed and variable amounts (2.5% + 30 cents, for example), small transactions can be more costly because the fee accounts for a larger proportion of the overall amount.

Tips to maximize your interchange revenue

As explained above, many factors influence the interchange rate, and most are outside your control. However, there are steps you can take to maximize your interchange revenue, including:

- Accepting all types of credit cards - credit cards can deliver more than double the interchange rates that debit cards can. Make sure to accept as many types of credit card as you can, including consumer, business, rewards, and premium cards, to take advantage of the different interchange rates for each type of card, and increase your overall interchange revenue.

- Targeting higher interchange fee transactions - there are a number of ways to do this. Firstly, card-not-present (CNP) transactions generate more interchange revenue, so the more online business you can do the better. Secondly, as certain product and service categories have higher fees than others, you should look to promote these categories through partnerships and marketing.

- Keeping chargebacks to a minimum - using the latest payment processing technologies and fraud prevention tools, complying with the latest card industry security standards, clearly communicating refund and return policies, maintaining accurate stock levels and product descriptions, and keeping a high level of customer service are great ways to reduce your risk of chargebacks, which helps to ensure that you receive the full interchange fee for each transaction.

- Utilizing data - using data analytics tools to monitor and analyze your transactions can help you understand how much of the interchange is coming to you and how much goes to your customers. This allows you to identify opportunities to optimize your payments process and maximize your interchange revenue.

- Negotiating with your acquirer - work with your acquirer to negotiate lower processing fees and access better interchange rates, which allows you to reduce costs and maximize interchange revenue.

How to start a card program and earn interchange revenue

Want to start a card program and start earning interchange revenue? Checkout.com can help with that. Our new Issuing product allows you to unlock new revenue by optimizing your physical or virtual card payment experience.

This flexible, end-to-end solution gives you full control of your card program and, as it’s highly scalable, can grow alongside your business. We offer a complete stack of issuing, processing and card management capabilities so you can supercharge your new card product and start earning quickly.

Check out our issuing product or contact us to learn more.

%20(1).png)

.png)