We spoke to leading payments experts, from enterprise merchants to our own payments engineers, to bring you a refreshed list of payments trends for the year ahead. Key themes include interoperability for cross-border commerce, agnostic architecture, network data mandates, strategic token management, and the agentic commerce revolution.

As we look ahead to 2026, the need for security and convenience in payments is as prevalent as ever. But with the current speed of technological innovation, the industry is transitioning from a phase of simple digitization to one of agentic intelligence and regulatory hardening. Offering a range of payment methods is no longer a differentiator. The competitive advantage now lies in how well payments perform: the rate at which legitimate payment attempts succeed on the first try, and the profitability of this function.

Let’s take a look at what 2026 holds for digital payments.

1. Better data in payment requests will drive revenue

As ecommerce matures, the ease of payment matters more than ever. Browsing through online stores is less common, as Similarweb put it, so “consumers arrive at retailer sites better informed and closer to purchase – raising the stakes for brands to capture conversion when the opportunity arises.”

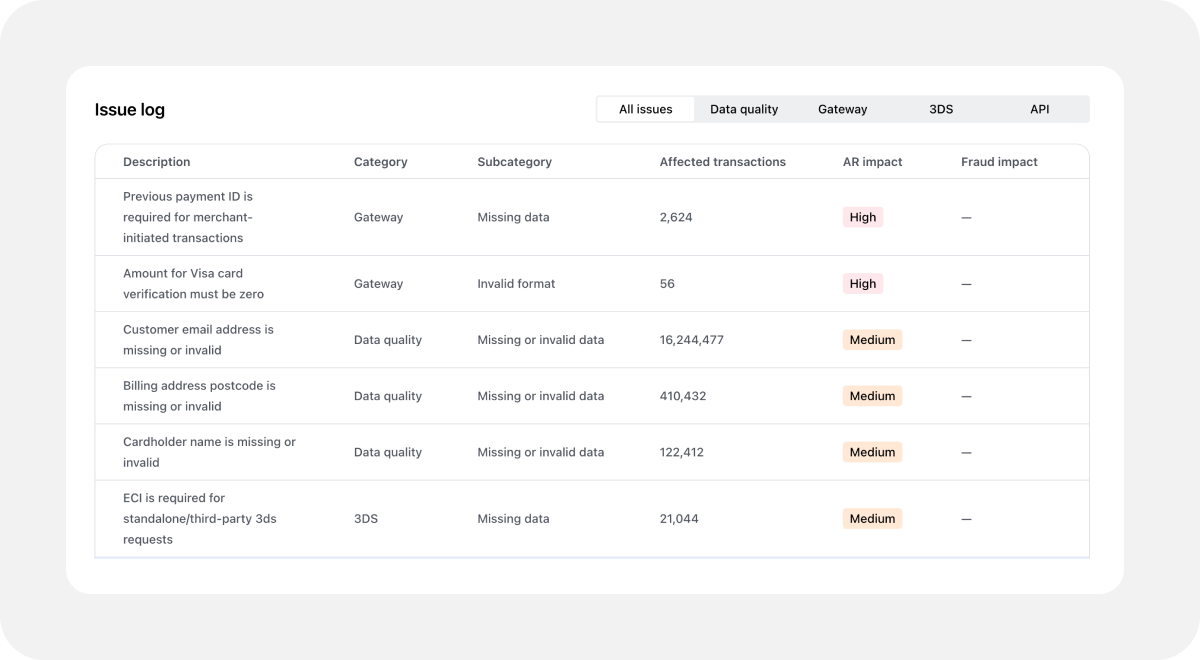

That’s why 2026 is the year to focus on data quality: submitting a payment request that contains all the necessary data for that payment to go through. When certain data fields are missing, issuers have less confidence in the transaction, which can trigger fraud blocking or blacklisting. That means a payment can fail for preventable reasons – and cause your customer to churn.

In April 2026, Visa will launch the Digital Commerce Authentication Program (VDCAP) in the US and Canada. This initiative incentivizes data quality: merchants providing specific data elements like Device ID, IP, Email, and Billing Address will qualify for a 0.05% fee reduction, rising to 0.10% if combined with Network Tokens in the US. In addition, as ISO 20022 mandates tighten in November, missing data fields will increasingly trigger hard declines rather than just soft failures.

Our analysis from 2025 confirms that improved data is already a lever for revenue recovery. Simply ensuring the IP Address field is populated drives an average acceptance rate increase of 0.35%, and including a validated Customer Email generates 0.26% more. While these gains seem marginal, applied to enterprise transaction volumes, they translate into millions in recovered revenue.

The penalty for poor data hygiene is escalating. Leading merchants are using tools like Integration Health not just to spot errors, but to proactively capture the full payload needed to secure these fee reductions and acceptance rate increases.

We know from extensive testing and validation that improved data quality improves fraud filtering accuracy and acceptance rates. Put simply, this year, focus on passing the right data for each payment to your payment services provider, and see your revenue grow.

2. Fraud detection tools will take on more sophisticated AI threats

The unfortunate downside of the AI explosion is its use by cybercriminals, which is set to continue throughout 2026. This is driving a more urgent need for AI-powered fraud prevention.

The benefits to strengthening your fraud strategy are self-explanatory: as well as protecting consumers from financial crime, your business will face fewer chargebacks and false declines. That means better cost efficiency in payment processing as well as higher customer satisfaction.

Careful fraud monitoring matters more in 2026 as schemes are introducing new fraud monitoring thresholds. For instance, the Visa Acquirer Monitoring Program (VAMP) now includes the total number of payment disputes coming through your business, and penalizes excessive enumeration attacks. Global thresholds come into effect in April. You can stay ahead of the changes by following our email updates or – if you’re a customer – talking to your account manager to see if you’re in line with current fraud thresholds.

Adaptive scoring and next-gen machine learning models actively improve your payment approval rate by reducing false positives while protecting your business from fraud risk. Fraud Detection Pro manages thresholds dynamically based on live model scores. This means reacting to a fraud attack as it happens and adjusting risk tolerance automatically, rather than waiting for a human analyst to write and deploy a new rule.

Our data validates this approach: merchants using our adaptive machine learning models have seen fraud reductions of up to 75% in verticals like iGaming and crypto.

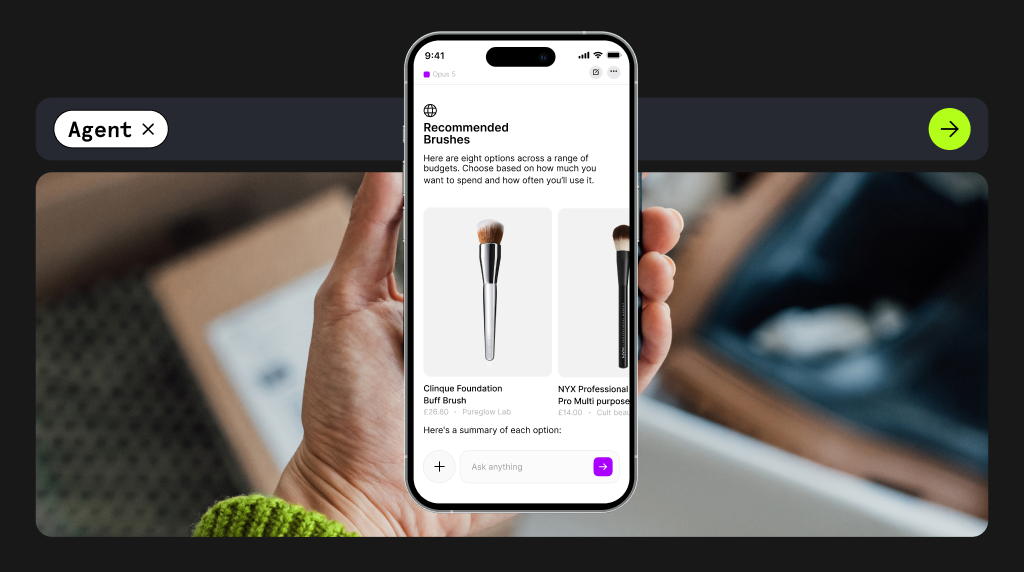

3. Agentic payments will move from hype to reality

If 2025 was the year of fanfare and hype, 2026 is the year merchants proactively connect to the growing agentic commerce infrastructure. Consumer interest is becoming concrete; our study of over 4,000 consumers found the average shopper is willing to spend $223 on a single agent-enabled purchase in the US, or £204.53 in the UK.

Global sales of B2C goods through AI agents are projected to reach up to $3-5 trillion by 2030, according to McKinsey. Capital investment reflects the growing momentum of agentic development, with AI drawing nearly a quarter of fintech funding in Q3 2025, per CB Insights.

Purchase-making bots are already online, billed as time-saving tools for busy consumers. Google rolled out ‘Buy for me’ in the US in November 2025, allowing users to track prices, trigger alerts, and make purchases from Wayfair, Chewy, Quince, and select Shopify merchants.

Amazon’s Rufus went even further: launching the same month as Google, its AI agent can purchase a product from its marketplace automatically once it hits the user’s desired price. Amazon found that consumers using its AI assistant were 60% more likely to complete a purchase.

Multiple protocols are emerging, with OpenAI’s Agentic Commerce Protocol (ACP) and Google’s Universal Commerce Protocol (UCP) gaining early prominence as a viable route for merchants to actively engage with this new shopping channel. Visa’s Intelligence Commerce (VIC) and Mastercard’s Agent Pay (MAP) are providing the tokenization services needed for secure, trustworthy AI payments.

The appearance of these different agentic models have the potential to create complexity – as well as risk that you may not invest in support for the right one at the right time. But at Checkout.com we’ve adopted protocols like OpenAI’s ACP and our payments experts are here to guide you through these new possibilities.

4. Network token strategies will unlock smoother payments

Mastercard’s 2030 deadline for full tokenization of ecommerce payments in Europe is fast approaching. As part of its own ecommerce vision, Visa is pushing for “ubiquitous tokenization” and citing up to 5% boost in authorization rates using its tokens. Payment tokenization – where the raw card numbers are replaced with a symbolic “token” in online transactions – is increasingly relevant in a world where the average US household is subscribed to 12 digital services.

Payment token strategy can be instrumental in reducing false declines. You can run experiments on different types of token provisioning (such as synchronous versus asynchronous) and dynamically apply them, to see which produce the best acceptance rates and business outcomes. In fact, experiments with token provisioning can produce tangible increases in authorization rate and reduced fraud.

On average, we observe an 11.7% increase in acceptance rates for tokenized transactions, compared to non-tokenized ones.

To guard against points of failure, it’s beneficial to use a dynamic decision engine that can switch between the token (DPAN) and the raw card number (FPAN) based on network performance, issuer preference, and machine learning. This will calculate the option with the highest probability of success, and improve the chances of each payment being accepted on the first attempt.

For increased control over your tokenization strategy, you may wish to look into decoupling your vault services from your token provider. This means you can manage your own tokens or shift tokens from one provider to another. For instance, the Vault from Checkout.com allows you to store payment credentials in a single location, and Forward API allows you to use them across multiple PSPs while remaining PCI-compliant.

Network tokens will also play a key role in agentic commerce; Visa launched its Trusted Agent Protocol in October, and has updated its network token provisioning to grant AI agents context-specific payment credential use.

5. Greater interoperability will reduce complexity in cross-border payments

At its core, interoperability allows different payment systems, services, and technologies to communicate and work together smoothly.

When payment systems can work together easily, businesses don’t have to build separate connections for every network. This makes payments faster, lower cost, and more competitive, and leaves room for innovation. It matters even more as businesses sell across borders and expect money to move instantly, at any time, and in any currency.

But the challenge is that banks, PSPs, and other payments players manage a complex tapestry of systems, technologies, scheme rules, and regulations that don’t always align around the world. Luckily, with the right communication and transparency, these systems can be connected. Overcoming different data standards, formatting, and legal frameworks requires technical, legal, and commercial agreements among a large group of international players in areas like currency conversion and Know Your Customer (KYC).

Regulators are reinforcing this trend. From eIDAS 2 interoperability in Europe to central bank initiatives like the digital pound, authorities are increasingly putting measures in place that position interoperability as essential to preserving trust, competition, and the singleness of money across payment types. Without it, new payment methods risk becoming isolated walled gardens, limiting choice and slowing innovation.

In 2026, interoperability becomes a strategic requirement for fast money movement. It allows you to connect both pay-ins and pay-outs through a single integration, reusing tokenized cards across both and managing balances in one place, regardless of the local scheme rules. This turns complexity into a competitive lever: the ability to move money locally and globally in minutes, while maintaining compliance and FX transparency through a unified infrastructure.

6. Agnostic architecture will liberate payments stacks

Payments work best when the PSP adapts to your existing architecture, not the other way around. This is agnostic architecture – the ability to decouple services, like vaulting, credential lifecycle enhancements, acquiring, and authentication, in a modular way that works for you. And it’s a big trend to watch this year.

As an enterprise business, there are countless pain points you could face in your payments stack. Complexity across markets or payment methods, authorization rate decline leading to revenue leakage, or balancing fraud prevention with a smooth customer experience.

By building a modular suite of specialized payment products and services in a custom configuration, you can solve immediate pain points without overhauling your entire stack.

One of the enablers of this trend is Standalone Vault. By tokenizing credentials once with one provider, like Checkout.com, and using those tokens to route transactions to any PSP, you can achieve true redundancy. This is crucial for resilience, because if your primary acquirer suffers an outage, you can automatically shift to your backup acquirer using the same stored credentials. It also means you can dynamically route the volume to the provider offering the best performance or price at that exact moment.

7. BNPL will drive even higher basket sizes

Fueled by the continued expansion of ecommerce, growing demand for flexible payment options, and strong adoption among younger, digital-native consumers like Gen Z, buy now, pay later (BNPL) is booming.

- $687 billion projected transaction value in 2028 (up from $334 billion in 2024)

- 900 million global consumers expected by 2027

In less than a decade, BNPL has fundamentally reshaped consumer behavior, evolving from a niche checkout option into one of the fastest growing alternative payment methods globally.

With this rapid growth, regulators around the world are stepping in to ensure consumers clearly understand BNPL’s borrowing implications and to prevent unsustainable debt. For businesses, this is a positive shift. It means credit and fraud risk increasingly sits with the BNPL provider, reducing your exposure.

What should you expect with BNPL in 2026? AI and embedded finance are integrating BNPL deeper into apps, moving usage beyond big-ticket items into everyday checkout experiences and increasing overall basket sizes.

Ultimately, BNPL remains a powerful revenue driver. Merchants of our partner, Alma, see a substantial 20% increase in average turnover and a 50% boost in basket size.

The focus for the year ahead is leveraging these regulated, tech-enabled credit options to capture customers who prefer flexible payments without carrying the risk on your balance sheet.

8. Stablecoins will become mainstream financial infrastructure

In 2024, the volume of on-chain stablecoin transactions hit $6 trillion, up from $1 trillion in 2020. That was before the milestone GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act) was signed into US law in July 2025, and the Markets in Crypto-Assets (MiCA) regulation was rolled out across EU member states throughout 2025. And where regulatory clarity is introduced, innovation and expansion follow.

Together, these regulations give stablecoins clear legal legitimacy and signal a new trend defined by trust and transparency. They both require stablecoins to be fully backed 1:1 by cash or cash equivalents, while balancing innovation with consumer protection. In doing so, they bring stablecoins closer to the trust standards expected of traditional money transmitters and accelerate adoption.

New regulations aren’t the only factor contributing to the growth of stablecoins. More stablecoins supply, driven by higher demand for digital currencies, means greater liquidity for real-time payments, and stablecoin solutions from the top payments players like PayPal, Visa, and Mastercard mean it’s easier than ever to accept stablecoin payments for your business.

Stablecoins offer access to programmable, global liquidity within a compliant framework, combining the efficiency of blockchain technology with the predictability of fiat-backed value. The result is near-real time settlement, lower transaction costs, and global reach, while complementing existing card and bank infrastructures.

The Fintech and Advanced Payments Report 2026 found that 45% of respondents see cross-border payments as the biggest impact of stablecoins, with 39% expecting strong use cases in B2B transactions. One of stablecoins’ clearest use cases is treasury management. Because stablecoins offer 24/7 settlement, your business could elect to be settled in stablecoins over weekends or holidays to maintain cash flow for inventory restocking or marketing spend.

Exploring stablecoin integrations today will help you shape how they fit into tomorrow’s use cases – from cross-border settlements and remittances to instant payouts – as this technology moves further into the mainstream.

9. The evolution of cards will create more opportunities to build loyalty

Traditional payment cards aren’t going away, but where they’re stored and how they’re used are changing.

Digital wallets like Apple Pay and Google Pay, virtual card numbers, and tokenization mean that identity in payments has become contextual and no longer tied to a single card number. Biometric authentication – like fingerprints or facial recognition – has further shifted identity away from the card and back toward the person, with the card acting as a silent intermediary.

Now, digital wallets are the preferred way to pay for consumers around the world, projected to account for 61% of total global ecommerce transaction value by 2027. The result of a mobile-first world.

This evolution allows you to use the payments experience to drive loyalty. Loyalty programs are moving directly into digital wallets, allowing consumers to earn and redeem rewards automatically at checkout based on real-time spending. In 2026, the opportunity lies in building co-branded initiatives where the "card" acts as a silent intermediary, and the value is delivered through a seamless, biometric-secured wallet experience.

Get ahead in 2026: Put a unified performance strategy into action

Last year, we predicted that payments in 2025 would be shaped by machine learning, smarter authentication, and a greater focus on efficiency (to name just a few). A lot of that progress has now become table stakes for enterprise payments teams.

What will define 2026 is more interconnected, and more demanding. The trends ahead all point to a single outcome: getting even more from every payment. That’s performance. It remains the most enduring opportunity in payments, but delivering it now requires a holistic view of the entire ecosystem.

Performance has moved on from improving one element in isolation. It’s determined by how data quality, fraud decisions, token strategies, and infrastructure work together across an increasingly complex environment, one that now includes emerging agent-led commerce.

Staying ahead means building resilient, data-rich payment flows that can evolve as new commerce models emerge. Disciplined use of granular data, AI, and modular architectures helps improve first-attempt success, reduce risk, and recover revenue at scale.

No matter what 2026 brings, our focus remains clear: solving the hardest challenges with real-world expertise, and helping payments deliver more to support your growth ambitions. If you’d like to explore what payments in 2026 mean for your business, what to prioritize, what to rethink, and where performance really comes from – we’re here to talk.

_How%20and%20why%20to%20launch%20a%20card%20program%20(1).png)

_Introducing%20Issuing.png)

.jpeg)